Many recipients struggle to navigate the maze of tax implications, manage the risk of having so much tied to one company, and decide on the right moment to hold or sell. This guide provides a clear roadmap for cutting through the complexity, helping you create a strategy to maximize the value of your equity awards and turn them into long-term financial security.

Key Takeaways

- Know the unique tax rules for your specific equity type (RSUs, ISOs, NSOs, ESPPs).

- Build a proactive tax plan to lower what you owe at vesting, exercise, and sale.

- Diversify your holdings to avoid over-concentration in a single company stock.

- Connect your equity strategy to major financial goals like retirement or a home purchase.

- Consult a specialist advisor to create a holistic, tax-efficient equity plan.

Understanding the Landscape of Equity Compensation

Equity compensation is a way for companies to give employees an ownership stake, aligning their personal financial success with the company's performance. It represents a promise of future value rather than immediate cash. Understanding the different forms is the first step toward making smart decisions.

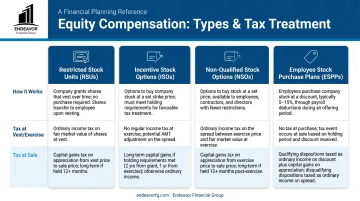

Common Types of Equity Awards

Restricted Stock Units (RSUs)

RSUs are the most straightforward form of equity. They are grants of company shares that you receive after meeting certain conditions, known as vesting. Vesting is typically based on time (e.g., staying with the company for a set number of years) or performance milestones. The moment your RSUs vest, their market value is taxed as ordinary income, just like your salary.

Incentive Stock Options (ISOs)

ISOs give you the right to buy company stock at a predetermined price, called the exercise price or strike price. Their main benefit is potential for favorable tax treatment. If you hold the stock for at least two years from the grant date and one year from the exercise date, your profit may be taxed at the lower long-term capital gains rate.

However, exercising ISOs can trigger the Alternative Minimum Tax (AMT), a parallel tax system that requires careful planning.

Non-Qualified Stock Options (NSOs)

Like ISOs, NSOs give you the right to purchase company stock at a set price, but the key difference is the tax treatment. When you exercise NSOs, the "bargain element"—the difference between the market price and your exercise price—is immediately taxed as ordinary income.

This tax is due whether you sell the shares or not. Any subsequent appreciation in value is then treated as a capital gain when you eventually sell.

Employee Stock Purchase Plans (ESPPs)

ESPPs allow you to buy company stock at a discount, often up to 15%, through convenient payroll deductions. Many plans include a "look-back" provision, which applies the discount to the stock price at either the beginning or the end of the offering period—whichever is lower.

This feature can significantly boost your returns. Like ISOs, ESPPs have specific holding period rules that determine whether your gains are taxed more favorably as long-term capital gains or as ordinary income.

Key Strategies for Maximizing Your Equity Benefits

Turning equity grants into actual wealth requires more than just waiting for a vesting date. It demands a deliberate strategy that balances growth potential, tax efficiency, and risk management.

Create a Proactive Tax Plan

Every action you take with your equity—vesting, exercising, or selling—has a tax consequence. A proactive plan helps you anticipate these costs and make decisions that minimize your overall tax burden. This involves forecasting your liability for ordinary income tax vs. long-term capital gains.

For instance, you might time the exercise of options or the sale of shares across different tax years to avoid pushing yourself into a higher tax bracket. Another strategy is tax-loss harvesting, where you sell other investments at a loss to offset the gains from your company stock. Under current federal rules, you can use capital losses to offset capital gains and up to $3,000 of ordinary income annually.

Develop a Diversification Strategy

Holding a large amount of your net worth in a single company's stock is a significant risk. Your salary, bonus, and portfolio are all tied to the same company's fate. If the stock price plummets, your financial security could be jeopardized.

The data on this is sobering. One J.P. Morgan study found that even seemingly healthy companies can experience a "catastrophic decline," defined as a 70% fall from its peak price without recovery.

Even more concerning, research from Dimensional Fund Advisors shows that over 20-year periods, only about one-fifth of individual stocks survive and outperform the broader market.

To mitigate this risk, create a systematic plan to sell shares over time. For executives and insiders, a Rule 10b5-1 plan can automate sales at predetermined times, providing a defense against insider trading allegations.

For other employees, simply selling a portion of RSUs as they vest and reinvesting the proceeds into a diversified portfolio can steadily reduce your concentration risk.

Align Equity Decisions with Your Financial Goals

Your equity is a tool to help you achieve your life goals. Instead of viewing it in isolation, integrate it into your broader financial plan.

- Buying a home? Earmark vested RSUs or proceeds from an option exercise for the down payment.

- Saving for college? A portion of your equity can be allocated to a 529 plan.

- Nearing retirement? Develop a multi-year strategy to gradually sell company stock and transition the funds into a more stable, income-focused retirement portfolio.

Understand Your Company's Rules and Blackout Periods

Always read your grant agreements carefully. They contain critical details about vesting schedules and expiration dates.

Be aware of any company-specific rules, such as trading windows or blackout periods (typically around earnings announcements), which restrict when you can sell shares. Missing a trading window could force you to hold your stock longer than planned, exposing you to unnecessary risk.

Optimize Your Exercise Strategy for Stock Options

With ISOs and NSOs, deciding when to exercise is a critical choice influenced by your cash flow, risk tolerance, and belief in the company's future.

- Exercise and hold: If you believe the stock will continue to appreciate and you have the cash to pay the exercise cost and any immediate taxes, you might exercise and hold. This strategy is often used with ISOs to qualify for long-term capital gains treatment.

- Cashless exercise and sell: If you need to limit your out-of-pocket costs, you can do a cashless exercise. In this transaction, a brokerage firm lends you the money to exercise your options, immediately sells enough shares to cover the cost and taxes, and deposits the remaining shares or cash into your account.

Common Pitfalls to Avoid in Equity Compensation Planning

Avoiding common mistakes is the first step to protecting your equity compensation. Many executives and employees watch their stock wealth evaporate by falling into these predictable traps.

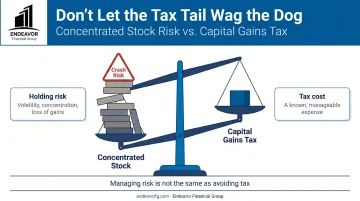

Letting the Tax "Tail" Wag the "Dog"

It's tempting to make decisions based only on tax avoidance. For instance, you might hold a highly appreciated stock indefinitely just to defer capital gains tax, but this can be a disastrous mistake.

The risk of a concentrated position crashing is often far greater than the tax bill you were trying to avoid. Your primary goal should be sound investment decisions, with tax efficiency as a secondary, but important, consideration.

Becoming Emotionally Attached to Company Stock

Working for a company can create a strong sense of loyalty and optimism about its future. This leads to what behavioral economists call the endowment effect—a tendency to overvalue something simply because you own it.

This bias can cloud your judgment, causing you to hold company stock for too long and ignore basic diversification principles. It's critical to evaluate your company stock with the same objectivity you would apply to any other investment.

Failing to Plan for the Associated Costs

Vesting RSUs or exercising NSOs can trigger a substantial, immediate tax bill. Without cash set aside to cover this liability, you might be forced to sell shares at an inopportune time just to pay the IRS.

Always calculate the estimated tax impact of any equity event before it happens and have a clear plan to meet that obligation.

How Endeavor Financial Group Can Help You Navigate Equity Compensation

Managing complex assets like equity compensation requires more than just investment advice—it demands comprehensive, strategic wealth planning. At Endeavor Financial Group, our specialists with CFP® and CFA® credentials build holistic plans that integrate your equity awards with tax planning, retirement goals, and risk management.

Our consultative, team-based approach ensures every decision aligns with your complete financial picture. We help create a clear roadmap for:

- Analyzing your specific grants—RSUs, ISOs, or NSOs—in the context of your total financial situation and risk tolerance.

- Developing tax-efficient strategies for exercising and selling shares in coordination with your tax professionals.

- Creating a disciplined diversification plan to reduce concentration risk and build a portfolio that supports your long-term goals.

Conclusion

Equity compensation is more than a bonus—it's a significant financial asset that requires careful management. By understanding your grants, planning for taxes, diversifying strategically, and aligning every decision with your life goals, you can make it a cornerstone of your long-term financial success.

Navigating these complexities on your own can be daunting. As fee-only fiduciary advisors, the team at Endeavor Financial Group provides the objective, comprehensive guidance needed to build a sound strategy. If you're ready for a clear roadmap for your equity compensation, contact us to get started.

Frequently Asked Questions

What are the main types of equity compensation?

The main types include RSUs (grants of company shares), ISOs/NSOs (options to buy shares at a set price), and ESPPs (plans to purchase company stock at a discount). Each has different rules and tax implications.

How much do financial advisors charge for equity compensation planning?

Fees vary, but common models include a percentage of assets under management (AUM), often around 1%, a flat fee for a comprehensive plan (typically starting around $3,000), or an hourly rate.

What are red flags when choosing a financial advisor for equity compensation planning?

Key red flags include advisors who are not fiduciaries, lack specific experience with equity compensation, push products before understanding your needs, or are not transparent about their fees.

What's the difference between vesting and exercising stock options?

Vesting is the process of earning the right to your options over time. Exercising is the separate action of actually purchasing the shares at the predetermined strike price once you are vested.

How does having a lot of company stock affect my overall financial risk?

It creates concentration risk. Having too much wealth in one stock exposes your portfolio to significant losses if that single company's stock price falls, linking your net worth directly to your employer's performance.

When is the best time to sell company stock?

There is no single "best" time. The right decision depends on your individual financial goals, tax situation, risk tolerance, and your confidence in the company's future performance.