Effective tax planning isn't about finding last-minute loopholes in April. It's a year-round discipline that transforms your tax bill from a liability into a tool for growth. This guide provides a comprehensive overview of actionable tax strategies, from foundational choices to advanced tactics, designed to help you keep more of your money where it belongs: in your business and your future.

Key Takeaways

- Select the right business entity (S-Corp, LLC) to build a strong tax foundation.

- Track and claim all eligible business deductions to maximize tax savings.

- Reduce taxable income using retirement plans like SEP IRAs and Solo 401(k)s.

- Make tax planning a year-round process through consistent record-keeping.

- Align your tax strategy with long-term wealth and business goals.

Foundational Strategies: Business Structure & Record-Keeping

Tax planning begins the moment you decide to start your business. The single most important decision you'll make early on is choosing your legal structure, as it directly dictates how your business is taxed.

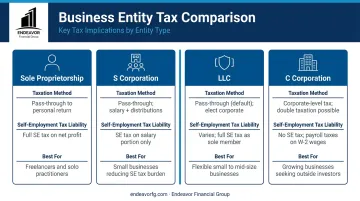

Choosing the Right Business Entity

Each business structure has unique tax implications. Understanding these differences is key to building an efficient foundation.

- Sole Proprietorship/Partnership: The default for unincorporated businesses. Profits and losses pass directly to your personal tax return (Schedule C), and you pay self-employment taxes on all net earnings.

- S Corporation (S-Corp): Offers pass-through taxation and can lower self-employment taxes. Owners must take a "reasonable salary" subject to payroll taxes, but additional profits can be withdrawn as distributions.

- Limited Liability Company (LLC): Provides liability protection with significant tax flexibility. An LLC can be taxed by default as a sole proprietorship/partnership or elect to be treated as an S-Corp or C-Corp.

- C Corporation (C-Corp): A separate tax-paying entity ideal for companies seeking venture capital. It faces potential "double taxation" but offers unique benefits like the Qualified Small Business Stock (QSBS) exclusion.

The Non-Negotiable Habit of Meticulous Record-Keeping

Tax deductions and credits are worthless if you can't prove them. Flawless record-keeping is the backbone of any successful tax strategy.

First, separate your business and personal finances immediately. Open a dedicated business bank account and credit card. Commingling funds is a recipe for accounting headaches and can put you at risk during an audit.

From day one, use accounting software like QuickBooks or Xero. Tracking every dollar of income and every expense as it happens makes tax preparation smoother and provides the real-time data needed for strategic decision-making throughout the year.

Maximizing Deductions and Credits: Your Key to Lowering Taxable Income

Lowering your tax bill starts with understanding the key difference between deductions and credits. A tax deduction lowers your taxable income, reducing your tax bill by a percentage based on your tax bracket. A tax credit is more powerful—it reduces your final tax liability dollar-for-dollar.

Common and Overlooked Business Deductions

Dozens of legitimate business expenses can be deducted, but a few key ones offer significant savings.

- Home Office Deduction: If you use a portion of your home exclusively and regularly for business, you can claim this deduction. You can use the simplified method ($5 per square foot, up to 300 sq. ft.) or the actual expense method, which includes a percentage of your mortgage interest, utilities, and repairs.

- Vehicle Expenses: When you use your car for business, you can deduct the costs. The easiest way is using the standard mileage rate set by the IRS, which for 2024 is 67 cents per mile. Because this rate changes, always verify the current figure. Alternatively, you can track all your actual expenses (gas, insurance, maintenance) and deduct the business-use percentage. Either way, you need a detailed mileage log.

- Startup and Organizational Costs: The IRS allows you to deduct up to $5,000 in startup costs and another $5,000 in organizational costs in your first year of business. Any costs above this amount are amortized over 15 years.

- Depreciation (Section 179 & Bonus Depreciation): Instead of depreciating assets over many years, Section 179 allows you to deduct the full purchase price of qualifying equipment and software in the year they are placed in service. For 2024, the deduction limit is $1,220,000. Bonus depreciation is also available for qualified property (at 60% for 2024), offering another powerful way to accelerate deductions.

Leveraging Powerful Tax Credits

Don't forget to explore tax credits, which can provide a significant direct reduction to your tax bill.

- Research and Development (R&D) Tax Credit: This isn't just for tech labs. If your business develops new products, processes, or software—even improving internal systems—you may qualify. It's one of the most underutilized credits by small businesses.

- Work Opportunity Tax Credit (WOTC): The federal government offers the WOTC to employers for hiring individuals from certain targeted groups, such as veterans, ex-felons, or recipients of government assistance.

Strategic Retirement & Compensation Planning

Your retirement and compensation strategies are not just expenses—they are key tools for reducing your current tax burden while building long-term wealth and retaining top talent.

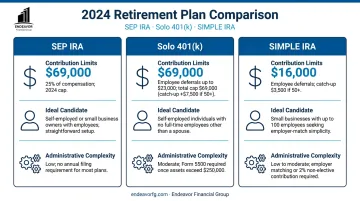

Reducing Your Taxable Income with Retirement Plans

Contributing to a retirement plan is one of the best ways for a business owner to lower their taxable income today.

- SEP IRA: Easy to administer and allows for significant, tax-deductible contributions. For 2024, you can contribute up to 25% of compensation, capped at $69,000.

- Solo 401(k): Ideal for owner-only businesses, allowing "employee" and "employer" contributions. In 2024, you can contribute up to $23,000 as an employee ($30,500 if 50+) plus an employer portion, with total contributions capped at $69,000.

- SIMPLE IRA: A great option for small businesses that includes both employee and employer contributions, making it an attractive and accessible benefit.

Tax-Efficient Compensation Strategies

How you pay yourself and your team also has major tax implications. S-Corp owners, for instance, must take a "reasonable salary" subject to payroll taxes. The key is balancing an amount that is defensible to the IRS without creating an excessive tax burden.

Paying employee bonuses before year-end is another effective strategy. If your business uses accrual-based accounting, you can often deduct these bonuses in the current tax year to lower your taxable income. Choosing the right approach requires careful planning.

Advanced Tax Planning: Timing, Gifting, and Year-End Moves

Proactive tax planning recognizes that when you make a financial move can be just as important as what move you make.

Timing Income and Expenses

A classic year-end strategy for cash-basis businesses is to manage the timing of income and expenses.

- Defer Income: If possible, you might delay sending invoices in late December so that the payments arrive in January, pushing that income into the next tax year.

- Accelerate Expenses: Conversely, you can pre-pay for expenses for the upcoming year—such as rent, insurance premiums, or professional subscriptions—in December to claim the deductions in the current tax year.

Beyond managing annual cash flow, long-term strategies play a crucial role in succession planning.

Strategic Gifting for Succession

For business owners thinking about succession, tax-smart gifting can be a valuable tool. The IRS allows you to gift a certain amount to any individual each year without triggering gift tax—for 2024, this annual exclusion is $18,000.

This strategy can be used to gradually transfer ownership stakes in the business to family members over time, reducing the future value of your taxable estate.

Why a Tax Strategy Needs a Wealth Plan: The Endeavor Approach

An effective tax strategy doesn't exist in a vacuum. It must be woven into the fabric of your broader financial life, including your investment strategy, retirement funding, and estate plan. Viewing taxes in isolation can lead to costly mistakes.

For example, aggressively taking every possible deduction to show the lowest possible net income might save you on taxes this year. However, that same low income could prevent you from qualifying for a mortgage or a crucial business loan you need for expansion next year.

This is where comprehensive planning from a firm like Endeavor Financial Group becomes critical. A tax preparer's job is to accurately report what happened last year, while our job is to proactively plan for the years ahead.

Our team of CFP® and CFA® professionals helps business owners build a cohesive strategy where tax planning supports, rather than conflicts with, long-term goals for financial freedom.

We believe nearly every financial decision has a tax implication. Our process ensures your tax strategy is integrated with your entire financial picture. We coordinate with your CPA to:

- Make tax-efficient investment choices.

- Structure your business properly for long-term advantages.

- Plan retirement withdrawals to minimize your lifetime tax bill.

This approach builds a single, unified plan that works for you, not just for the IRS.

Frequently Asked Questions

What is the first step in tax planning for a small business?

The first step is choosing the right legal entity (e.g., LLC, S-Corp) for your situation. Immediately after, you should open a separate business bank account to keep finances organized and protected.

How can I reduce my taxable income as a business owner?

The primary methods are maximizing all eligible business deductions, making tax-deductible contributions to retirement plans like a SEP IRA or Solo 401(k), and operating under a tax-efficient business structure.

Do I need a separate bank account for my small business?

Yes, a separate account is crucial for accurate bookkeeping and protecting your personal assets from business liabilities. It also prevents commingling funds, which can create significant legal and tax problems.

What is the difference between a tax deduction and a tax credit?

A deduction reduces your taxable income, lowering your tax bill based on your tax bracket. A credit provides a dollar-for-dollar reduction of your final tax bill, which makes credits more valuable than deductions of the same amount.

Can I pay myself a salary from my LLC or S-Corp?

If you own an S-Corp and work in the business, you are required to pay yourself a "reasonable salary." Members of a standard LLC typically take owner's draws, not a salary, unless the LLC has formally elected to be taxed as an S-Corp.

When should I consult a professional for tax planning?

You should consult a professional right from the start to help with entity selection. After that, an annual strategy session is wise, especially as your business grows, your personal situation changes, or tax laws are updated.