Long-Term Care Financial Planning: A Complete Guide

John, a successful business owner in his late 50s, felt he had his retirement plan locked down. He’d maxed out his 401(k) for decades and built a healthy investment portfolio.

But when his wife had an unexpected health crisis that required round-the-clock assistance, their financial world was turned upside down. The cost of her care—an expense they never planned for—began to drain their savings at an alarming rate.

This scenario is far too common. Many diligent savers focus on accumulating wealth but overlook one of the single largest potential expenses in retirement: long-term care. Without a strategy, a lifetime of hard work can be eroded in just a few years.

This guide will walk you through the realities of long-term care, from the staggering costs to the funding options available. We’ll provide a clear framework to help you build a plan that protects your assets, secures your future, and gives you confidence in your financial future.

Long-Term Care Planning at a Glance

- Long-term care is non-medical assistance with daily activities (bathing, dressing) and is needed by an estimated 70% of people over 65.

- Standard health insurance and Medicare do not cover a majority of long-term care costs, leaving a significant financial gap.

- Funding options include self-funding, long-term care insurance (traditional or hybrid), and government programs like Medicaid (with strict asset limits).

- Proactive planning, ideally in your 50s, is crucial to access more options at a lower cost, protecting your retirement savings and legacy.

What is Long-Term Care and Why is Planning Essential?

Many people confuse long-term care (LTC) with medical care, but they are fundamentally different. Understanding this distinction is the first step in effective financial planning.

Defining Long-Term Care (LTC)

Long-term care is not about doctors, hospitals, or prescriptions. It’s primarily custodial care, which means help with Activities of Daily Living (ADLs). These are the basic tasks of self-care that healthy, active people do without a second thought.

Common ADLs include:

- Bathing and showering

- Dressing and grooming

- Eating

- Getting in and out of a bed or chair (transferring)

- Using the toilet

LTC also includes supervision and support for individuals with cognitive impairments, such as Alzheimer's disease or dementia. This care can be provided in several settings, including at home by family or a professional aide, in an assisted living facility, or in a nursing home.

The High Probability of Needing Care

The need for long-term care isn't a remote possibility; it's a statistical likelihood. According to the U.S. Department of Health and Human Services, someone turning 65 today has almost a 70% chance of needing some form of long-term care in their lifetime.

Ignoring this probability is like building a retirement plan without accounting for inflation. It leaves a massive, predictable hole in your financial strategy.

The Sobering Reality: Understanding the Costs of Long-Term Care

The primary reason long-term care planning is so critical comes down to one thing: the cost. An extended need for care can become one of the most significant threats to your retirement portfolio, with expenses easily surpassing six figures annually.

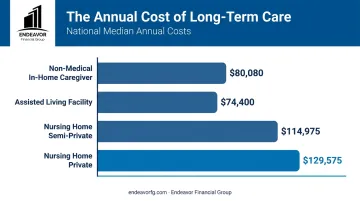

According to the 2025 Cost of Care Survey by CareScout, the national median costs for care are significant:

- Non-Medical In-Home Caregiver: $80,080 per year

- Assisted Living Facility: $74,400 per year

- Nursing Home (Semi-Private Room): $114,975 per year

- Nursing Home (Private Room): $129,575 per year

These are national medians, and costs can vary dramatically depending on where you live. For residents here in Indiana, it's crucial to research local figures to get a more accurate picture of your potential expenses.

Facing these numbers without a plan could force you to liquidate assets you intended for your spouse or heirs.

Debunking the Biggest Myth: What Medicare and Health Insurance Don't Cover

One of the most dangerous misconceptions about retirement planning is the belief that Medicare will cover long-term care expenses. It will not.

Medicare is a health insurance program for medical needs, not a funding source for long-term custodial care. Its coverage for nursing facility care is extremely limited and comes with strict requirements:

- It’s short-term. Medicare only covers up to 100 days of skilled nursing care per benefit period.

- It requires a qualifying hospital stay. You must have been admitted as a hospital inpatient for at least three consecutive days.

- It’s not free. For 2026, after the first 20 days, there is a daily coinsurance of $217 (this amount typically changes each year). After day 100, you are responsible for all costs.

- It excludes custodial care. If your care needs are primarily for help with ADLs and not skilled medical services, Medicare provides no coverage.

Likewise, your standard health insurance policy is designed for doctor visits, hospital stays, and prescriptions. It explicitly excludes coverage for non-medical, custodial long-term care. Believing otherwise is a financial gamble you can't afford to lose.

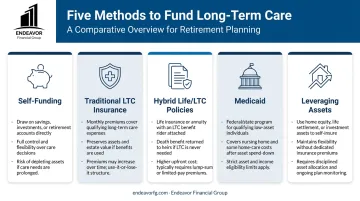

Your Financial Toolkit: Exploring 5 Ways to Fund Long-Term Care

Once you accept that you'll likely be responsible for the cost, the next step is to understand your funding options. Each approach has distinct advantages and disadvantages, and a fiduciary financial planner can help you build a strategy that fits your goals.

1. Self-Funding (Paying Out-of-Pocket)

This is the default strategy for those who don't plan. It involves using personal assets—savings, brokerage accounts, IRAs, or 401(k)s—to pay for care as the need arises. While this offers flexibility, it puts your entire nest egg at risk. Pulling large sums from tax-deferred accounts like a traditional IRA can also trigger a significant income tax bill, depleting your funds even faster.

2. Traditional Long-Term Care Insurance

With a traditional LTC policy, you pay regular premiums to an insurance company. In return, if you need care and meet the policy's criteria (typically being unable to perform two or more ADLs), the policy pays a pre-determined daily or monthly benefit up to a lifetime maximum. Modern policies often include features like inflation protection to ensure your benefits keep pace with rising costs.

3. Hybrid Life Insurance/LTC Policies

A popular alternative is a hybrid policy that combines life insurance with a long-term care rider. This design allows you to accelerate a portion of the policy's death benefit, tax-free, to pay for qualified LTC expenses.

The key advantage is that the premium serves a dual purpose. If you never need long-term care, your heirs receive the full death benefit, eliminating the "use it or lose it" dilemma of traditional LTC insurance.

4. Government Assistance (Medicaid)

Medicaid is the payer of last resort, not a proactive planning tool. It's a federal and state program that covers LTC costs for individuals with very low income and minimal assets.

To qualify, you must first "spend down" nearly all of your savings, leaving very little for a surviving spouse or your heirs. This approach means relinquishing control over your assets and care choices.

5. Leveraging Other Assets

Beyond the primary methods, other financial tools can play a role:

- Annuities: Some annuities offer riders that can double your payout for a set period to cover LTC expenses.

- Home Equity: A reverse mortgage or home equity line of credit (HELOC) can convert your home's value into cash for care, but this reduces the asset's value for your heirs.

- Health Savings Accounts (HSAs): If you have an HSA, the funds can be used tax-free to pay for qualified long-term care services including some LTC insurance premiums.

Building Your Personalized LTC Financial Strategy

Knowing your options is the first step. The next is building a strategy that fits your unique financial situation, health profile, and personal preferences.

Assess Your Potential Need and Preferences Look at your family's health history. Are there genetic predispositions to conditions like dementia or Parkinson's? Consider your own health and lifestyle. Equally important, think about your preferences. Do you want to receive care at home for as long as possible, or would you prefer a community setting?

Calculate Your Potential Funding Gap Using the cost data as a baseline, estimate your potential future LTC expenses. Compare this figure to the resources you have available to self-fund without derailing your other financial goals. The difference is your funding gap—the amount you need a dedicated strategy to cover.

Evaluate and Select Your Funding Tools The best plan often involves a layered approach. You might decide to self-fund the first year of care (acting as a deductible) and use an insurance policy to cover a catastrophic, multi-year event. Your age, health, and risk tolerance will help determine whether a traditional or hybrid policy makes more sense.

Integrate LTC into Your Overall Financial Plan Long-term care planning cannot happen in a silo. It must be woven into your retirement income strategy, investment portfolio, and estate plan. A decision to self-fund, for example, directly impacts the assets available for your heirs and the income stream available for your spouse.

Work with a Professional to Formalize Your Plan Navigating these options is complex. The financial and tax implications of each choice are significant, and a misstep can be costly. Working with a qualified financial advisor is essential to making an informed decision.

As a fee-only fiduciary firm, Endeavor Financial Group specializes in this type of comprehensive planning. Because we don't sell insurance products, our legal and ethical duty is to provide objective advice that serves your best interest.

We use a structured process to analyze your complete financial picture, identify potential gaps, and build an actionable roadmap. By coordinating with your tax and legal professionals, we ensure your LTC strategy works in harmony with all your other financial goals.

Frequently Asked Questions

What is long-term care financial planning?

It is the process of creating a strategy to pay for future long-term care costs. The goal is to do so without depleting your retirement savings, selling off assets you want to leave to heirs, or burdening your family members.

At what age should I start planning for long-term care?

The ideal time is typically in your early to mid-50s. At this age, you are more likely to be healthy enough to qualify for insurance, and the premiums will be significantly more affordable than if you wait until your 60s or 70s.

Will my regular health insurance cover the cost of long-term care?

No. Standard health insurance is for medical care like doctor visits and hospitalizations. Long-term care is custodial (non-medical) and requires a separate funding strategy or a specific long-term care insurance policy.

What happens if I run out of money to pay for long-term care?

Once your personal assets are depleted to a state-mandated level, you may become eligible for Medicaid. This joint state and federal program covers LTC costs for individuals who meet strict financial need requirements.

Can I use my 401(k) or IRA to pay for long-term care?

Yes, you can use these funds to pay for care. However, withdrawals from traditional (pre-tax) retirement accounts are typically taxed as ordinary income, which can create a large tax liability in the years you need the money most.

How does a long-term care plan protect my assets for my heirs?

By using tools like insurance to cover the high cost of care, you avoid having to sell off your home, investments, or other assets intended for your estate. This preserves the legacy you worked so hard to build for your loved ones.