Many successful professionals and business owners overlook the power of "tax drag," the silent reduction of investment returns caused by taxes. Over decades, this can erode a significant portion of your nest egg. This guide provides a clear roadmap to foundational strategies, advanced techniques, and holistic planning to help you keep more of your hard-earned money for the retirement you deserve.

TL;DR: Key Retirement Tax Strategies for High Earners

- Maximize contributions to tax-advantaged accounts like 401(k)s and HSAs.

- Use Backdoor and Mega Backdoor Roth conversions to bypass income limits.

- Employ tax-efficient investment strategies like asset location and tax-loss harvesting.

- Use strategic philanthropy, such as Qualified Charitable Distributions (QCDs), to reduce taxable income.

- Develop a cohesive plan with a financial professional to coordinate these strategies.

Foundational Strategies: Maximizing Tax-Advantaged Accounts

Before exploring advanced techniques, mastering the fundamentals is essential. These accounts are the building blocks of any effective retirement tax strategy.

Your Workplace Retirement Plan (401(k), 403(b))

Your employer-sponsored retirement plan is your first line of defense against taxes. For 2026, you can contribute up to $24,500 to your 401(k) or 403(b). Making the maximum pre-tax contribution lowers your taxable income for the year, providing an immediate and significant tax benefit.

Many plans also offer a Roth 401(k) option, where you contribute after-tax dollars. While there's no upfront deduction, your investments grow tax-free, and qualified withdrawals in retirement are also completely tax-free.

This can be a powerful choice if you expect to be in an equal or higher tax bracket during your retirement years.

If you are age 50 or over, you can make additional "catch-up" contributions. For 2026, this amount is generally $8,000. However, due to new rules, if your prior-year W-2 wages exceeded $150,000, these catch-up contributions must be made on a Roth (after-tax) basis.

Health Savings Accounts (HSAs): A Triple-Tax-Advantaged Tool

A Health Savings Account (HSA) is often overlooked as a retirement tool, but it offers a unique triple tax advantage:

- Tax-deductible contributions: Your contributions reduce your current taxable income.

- Tax-free growth: The money in your HSA can be invested and grows without being taxed.

- Tax-free withdrawals: You can withdraw funds tax-free at any time for qualified medical expenses.

For 2026, individuals with a high-deductible health plan can contribute up to $4,400 to an HSA, while families can contribute up to $8,750.

By paying for current medical expenses out-of-pocket and allowing your HSA funds to grow, you can build a substantial, tax-free account to cover healthcare costs in retirement.

Retirement Plans for Business Owners and the Self-Employed

If you're a business owner or self-employed, you have access to even more powerful tax-advantaged savings vehicles. A SEP IRA allows you to contribute a significant portion of your compensation, while a SIMPLE IRA is a straightforward option for small businesses. Both allow for large, tax-deductible contributions that can dramatically reduce your current tax liability.

Advanced Contribution Strategies for High Earners

Once your income exceeds certain thresholds, the IRS limits your ability to contribute directly to some of the most beneficial accounts. Fortunately, there are legitimate, IRS-sanctioned strategies to get around these limitations.

The Backdoor Roth IRA

Direct contributions to a Roth IRA are phased out for high earners, with the 2026 limit for married couples filing jointly starting at $242,000 of Modified Adjusted Gross Income (MAGI). The Backdoor Roth IRA is a two-step process to bypass this:

- Contribute to a Traditional IRA: You make a non-deductible contribution to a Traditional IRA. Since you are a high-income earner with a workplace plan, you likely can't deduct this contribution anyway.

- Convert to a Roth IRA: Shortly after, you convert the funds from the Traditional IRA to a Roth IRA. You'll only pay tax on any earnings that may have accrued between the contribution and the conversion.

A critical consideration is the pro-rata rule. If you have other pre-tax IRA assets, such as from a previous 401(k) rollover, the IRS requires any conversion to be a proportional mix of your pre-tax and after-tax dollars.

This can trigger a significant tax bill, making the Backdoor Roth most effective for individuals with no existing pre-tax IRA balances.

While the Backdoor Roth is a powerful tool for IRA contributions, an even more potent strategy exists for those with accommodating 401(k) plans.

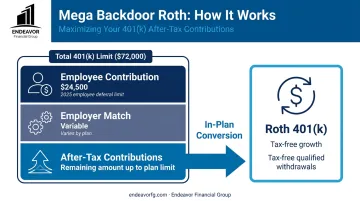

The Mega Backdoor Roth

This is an even more powerful strategy available to those whose 401(k) plan allows for two key features: after-tax (non-Roth) contributions and in-plan Roth conversions. The total amount you and your employer can contribute to your 401(k) in 2026 is $72,000.

After maxing out your standard pre-tax or Roth 401(k) contribution ($24,500 for 2026) and receiving an employer match, you may still have room to contribute after-tax dollars up to the $72,000 annual limit.

You can then immediately convert those after-tax contributions into the Roth 401(k) portion of your plan, allowing a massive amount of money to grow tax-free for retirement.

Beyond 401(k)s, some high-income professionals can use a different type of plan to save even more aggressively.

Cash Balance Plans

For successful business owners and high-income professionals, a cash balance plan offers a significant advantage. This type of defined benefit plan can be layered on top of a 401(k), allowing for very large, tax-deductible contributions determined by an actuary.

It's not uncommon for a 50-year-old business owner to contribute over $150,000 per year. This provides a massive immediate tax deduction while rapidly accelerating retirement savings.

Tax-Efficient Investing and Withdrawal Tactics

How you invest and withdraw your money is just as important as how you save it. These tactics focus on minimizing the tax impact on your portfolio's growth and your retirement income.

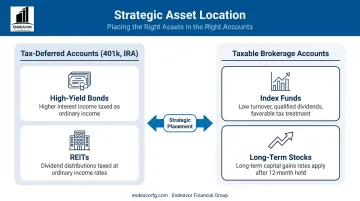

Strategic Asset Location

Asset location is the practice of placing different types of investments into the accounts that provide the most favorable tax treatment.

- Tax-Deferred Accounts (401(k), Traditional IRA): These are best for tax-inefficient investments. Assets that generate a lot of annual taxable income, like high-yield corporate bonds and REITs, can grow without creating a yearly tax bill inside these accounts.

- Taxable Brokerage Accounts: These are ideal for tax-efficient investments. Assets like index funds or individual stocks held for the long term generate lower taxes (preferential long-term capital gains rates) and can benefit from strategies like tax-loss harvesting.

Managing Capital Gains

Not all investment gains are taxed equally. The difference is critical for high earners.

- Short-Term Capital Gains: On assets held for one year or less, gains are taxed at your ordinary income tax rate, which can be as high as 37%.

- Long-Term Capital Gains: On assets held for more than one year, gains are taxed at lower preferential rates of 0%, 15%, or 20%.

The goal is simple: hold appreciated assets for at least a year and a day before selling. You can also use tax-loss harvesting, which involves selling investments at a loss to offset gains realized elsewhere in your portfolio. If your losses exceed your gains, you can deduct up to $3,000 per year against your ordinary income.

Planning for Required Minimum Distributions (RMDs)

At age 73, the IRS requires you to start taking Required Minimum Distributions (RMDs) from your tax-deferred retirement accounts. For high earners with large balances, these forced withdrawals can create a "tax torpedo," pushing you into a higher tax bracket during retirement.

One key strategy is to use your "gap years"—the time between retirement and when RMDs begin—to make partial Roth conversions. This involves moving funds from a traditional IRA or 401(k) to a Roth account.

By converting funds during these potentially lower-income years, you can pay taxes at a more favorable rate. This reduces the balance subject to future RMDs and builds a source of tax-free income for later in life.

Investing in Tax-Advantaged Vehicles

For assets in a taxable brokerage account, municipal bonds are an attractive option. The interest income they generate is typically exempt from federal income tax.

If you invest in bonds issued within your home state, the interest may also be exempt from state and local taxes. This can create a completely tax-free income stream.

Strategic Wealth Transfer: Philanthropy and Estate Planning

Your financial legacy is about more than just investments. Strategic giving and estate planning can be powerful tools for reducing your overall tax burden while supporting the people and causes you care about.

Tax-Smart Charitable Giving with Qualified Charitable Distributions (QCDs)

If you are age 70½ or older, you can use a Qualified Charitable Distribution (QCD) to donate directly from your IRA to a qualified charity. For 2026, you can donate up to $111,000 per year.

The primary benefit is that the QCD amount is excluded from your adjusted gross income (AGI). Better yet, it can be used to satisfy all or part of your RMD for the year. This allows you to support your favorite charities while simultaneously reducing your taxable income.

Using Trusts for Tax Efficiency

Trusts are legal arrangements that help you manage assets, provide for heirs, and reduce the size of your taxable estate. Different types of trusts can achieve specific tax-efficiency goals:

- Charitable Remainder Trust (CRT): Provides you with an income stream for a set period. The remaining assets go to a charity, giving you an immediate deduction and removing them from your estate.

- Spousal Lifetime Access Trust (SLAT): Moves assets out of your estate while still providing potential benefits for your spouse.

Annual Gifting Strategy

One of the simplest ways to reduce your future estate tax liability is to gift assets during your lifetime. For 2026, the IRS allows you to give up to $19,000 per person to as many individuals as you like without filing a gift tax return.

A married couple can combine their exclusions to give up to $38,000 per recipient. Over many years, this strategy can transfer significant wealth to the next generation completely tax-free.

These strategies often involve complex legal and financial coordination. Working with a financial advisor alongside your tax and legal professionals ensures your estate plan aligns with your overall wealth management goals.

Putting It All Together: Creating Your Holistic Retirement Tax Strategy

The strategies discussed here are powerful, but they are not standalone tactics. A Backdoor Roth IRA on its own is useful, but its true power is unlocked when coordinated with asset location, RMD planning, and your overall estate plan. The right mix depends on your unique circumstances, including your age, income, goals, and state of residence.

Navigating this complexity requires expert guidance. A piecemeal approach can lead to different parts of your financial life working against each other, creating costly mistakes.

At Endeavor Financial Group, we use a consultative, holistic approach to build a personalized roadmap. As a fee-only fiduciary, our advice is legally bound to your best interests and free from the conflicts of interest found in commission-based models. Our five-step process ensures all pieces of your financial plan work in concert.

Our CFP® designated advisors specialize in the complex needs of pre-retirees and business owners, creating integrated plans that maximize tax efficiency. If you're ready to build a strategic wealth plan that protects your assets and secures your future, we're here to help.

Contact Endeavor Financial Group today to start building your strategic wealth plan.

Frequently Asked Questions

What are the best retirement tax strategies for high income earners?

Key strategies include maximizing tax-advantaged accounts (401k, HSA), using backdoor Roth conversions for tax-free growth, and practicing tax-loss harvesting. Proactively planning for RMDs with strategic Roth conversions is also crucial.

What is a backdoor Roth IRA and why is it important for high earners?

A backdoor Roth IRA is a strategy for high earners to bypass income limits and fund a Roth IRA. It involves converting a non-deductible Traditional IRA contribution, which enables tax-free investment growth and withdrawals in retirement.

How can I reduce taxes on my required minimum distributions (RMDs)?

You can use Qualified Charitable Distributions (QCDs) to donate from your IRA, excluding that amount from your income. Another tactic is to perform strategic Roth conversions in the years before RMDs begin to lower the account balance subject to withdrawal.

When should I consider a Roth conversion?

The best time for a Roth conversion is typically in a lower-income year. This could be early in retirement before RMDs begin, during a sabbatical, or in a market downturn when asset values are temporarily lower.

What expenses are 100% write-offs?

For business owners, "ordinary and necessary" expenses are fully deductible. This includes costs like software, office supplies, professional fees, and marketing that are directly related to operating your business.

How do trusts help with taxes in retirement?

Irrevocable trusts can remove assets from your taxable estate, reducing or eliminating estate taxes for your heirs. They can also shift income-generating assets to beneficiaries in lower tax brackets to minimize the family's overall tax liability.