Making these decisions can be stressful. You’re not just assigning tasks; you're placing your family's financial future and well-being in someone else's hands. This is one of the most critical choices you'll make, and it deserves careful thought.

This guide is here to help. We'll walk through what a fiduciary is, the different roles they play, their legal responsibilities, and how to select the right people or institutions to protect your assets and beneficiaries.

TL;DR: Key Fiduciary Takeaways

- A fiduciary is legally and ethically required to act in your best interest.

- Key roles include Personal Representative (Executor), Trustee, and Agents for financial and health care powers of attorney.

- All fiduciaries must uphold the duties of loyalty (no self-dealing) and care (prudent management).

- Choosing a fiduciary requires evaluating trust, financial sense, availability, and impartiality—not just family ties.

- Breaching these duties can lead to personal financial liability and removal by a court.

What is a Fiduciary in Estate Planning?

In simple terms, a fiduciary is a person or entity legally and ethically bound to act in the best interests of another party. In estate planning, this means they must manage your assets and carry out your instructions for the benefit of your heirs and beneficiaries.

The entire relationship is built on a foundation of trust, loyalty, and good faith. This is fundamentally different from a typical "arm's-length" transaction where parties are expected to act in their own self-interest. A fiduciary's own interests must always come second.

An effective analogy is a ship's captain, who is responsible for the vessel and everyone on board. A fiduciary holds a similar duty for the "ship" of your estate and the well-being of its "crew"—your beneficiaries.

Their primary job is to navigate challenges and bring the estate safely to its destination, following the course you've charted in your plan.

The Key Fiduciary Roles in Your Estate Plan

Your estate plan will likely involve several fiduciaries, each with a distinct job. Understanding these roles—including the personal representative, trustee, and power of attorney agents—is the first step to choosing the right person for each one.

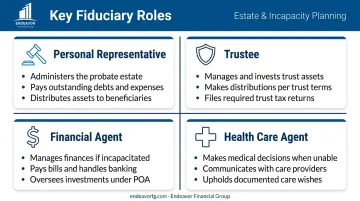

Personal Representative (or Executor)

Appointed in your will, the personal representative is responsible for administering your probate estate after you pass away. This is a temporary but intensive role focused on settling your final affairs.

Primary responsibilities include:

- Gather and inventory all estate assets.

- File the will with the appropriate court to begin probate.

- Notify heirs and creditors.

- Pay outstanding debts, bills, and final taxes.

- Distribute the remaining property to heirs as specified in the will.

Trustee

A trustee manages assets held within a trust. Unlike a personal representative, a trustee's role can be long-term, sometimes lasting for many years or even decades, depending on the terms you set.

Key duties of a trustee often involve:

- Invest and manage trust assets prudently.

- Make distributions to beneficiaries according to the trust document (which can be mandatory or discretionary).

- Keep detailed records of all transactions.

- File annual fiduciary income tax returns for the trust.

- Provide regular accountings and communicating with beneficiaries.

Agent under a Financial Power of Attorney

This person is your appointed agent to manage your financial affairs if you become incapacitated and are unable to do so yourself. Because they have significant control over your assets while you are living, this role requires absolute trust.

Their authority can be broad and may include:

- Manage bank accounts and paying bills.

- Buy or sell real estate.

- Manage investment portfolios.

- File your personal income taxes.

- Operate a small business.

Agent under a Health Care Power of Attorney (Health Care Proxy)

A health care agent makes medical decisions on your behalf if you cannot communicate your wishes. This person should be someone who understands your values and can advocate for you in a stressful medical environment.

Their responsibilities include:

- Communicate with doctors and medical staff.

- Access your medical records.

- Consent to or refusing medical treatments, tests, or procedures.

- Make end-of-life decisions based on your directives in a living will.

Selecting the right individuals for these positions is one of the most critical aspects of effective estate planning. A financial advisor can help you think through the qualifications needed for each role and coordinate with your attorney to ensure your plan is managed by fiduciaries you can trust.

Understanding the Core Fiduciary Duties

Regardless of their specific title, all fiduciaries are held to a high legal standard. Their actions are governed by two primary duties that form the bedrock of their responsibilities.

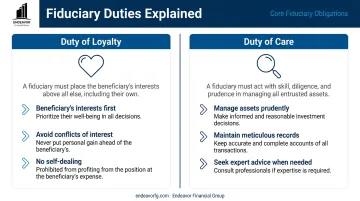

The Duty of Loyalty

The most fundamental fiduciary duty is loyalty. According to The Florida Bar, this duty requires the fiduciary to put the beneficiary's interests first, ahead of their own. This means they must avoid any and all conflicts of interest and can never use their position for personal gain.

A classic example of a breach of loyalty is self-dealing. A trustee cannot sell a home from the trust to themselves at a below-market price, because that would benefit them at the expense of the beneficiaries. Any transaction between the fiduciary and the estate must be fair and transparent, and in many cases, it requires court approval.

The Duty of Care (and Prudence)

Fiduciaries also have a duty of care, which means they must manage the estate's affairs with the skill and prudence a reasonable person would use for their own matters. This isn't just about avoiding mistakes; it's about actively and competently managing the assets under their control.

A key part of this duty is recognizing when to seek expert help. As the American Bar Association notes, a fiduciary without financial experience should seek professional advice on investing assets to meet their legal obligations. Other core responsibilities include:

- Maintaining meticulous records of every transaction, decision, and communication.

- Protecting and preserving all estate property.

- Following the "prudent investor rule" to make sound investment decisions.

How to Choose the Right Fiduciary for Your Legacy

Selecting your fiduciaries is a decision that requires more thought than simply naming your oldest child or a close friend. The right choice can ensure your plan runs smoothly, while the wrong one can lead to family conflict and financial loss.

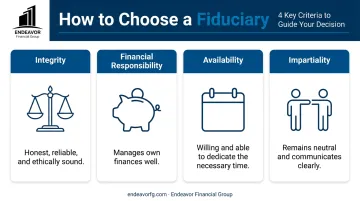

Consider these key criteria for every role you fill:

- Look for unwavering integrity. This is the non-negotiable foundation. Your fiduciary must be honest, reliable, and ethically sound.

- Assess their financial responsibility. Your appointee should manage their own finances well. For complex estates, they may need more sophisticated financial acumen.

- Confirm their willingness and availability. Executor and trustee roles are time-consuming. Ensure your choice is willing to accept and that their age, health, and location are suitable.

- Prioritize impartiality and communication. A good fiduciary remains neutral during family disagreements and communicates clearly with all beneficiaries.

Beyond these personal traits, you also face a structural choice: appointing an individual versus a corporate fiduciary.

An individual, such as a family member, knows your family best. However, a professional fiduciary offers specialized expertise, guaranteed impartiality, and continuity. While they charge a fee, their involvement can prevent costly errors and family disputes.

What Happens When a Fiduciary Breaches Their Duty?

When a fiduciary fails to uphold their duties, whether through intentional misconduct or negligence, it's called a breach of duty. Beneficiaries who suspect a breach have legal recourse to protect the estate.

Examples of breaches include:

- Self-dealing: Using estate assets for personal benefit.

- Negligence: Making poor investment decisions that lose money or failing to pay taxes on time.

- Commingling: Mixing estate assets with their own personal funds.

- Failing to Account: Not providing beneficiaries with a clear accounting of the estate's finances.

A fiduciary who commits a breach can face serious consequences. A court can order them to repay any financial losses they caused. For example, Virginia law states that a trustee who breaches their trust is liable for the amount required to restore the trust's value plus any profit they made from the breach.

The court can also remove them from their position and deny any compensation they might have received.

How Endeavor Financial Group Helps Align Your Fiduciary Choices

Choosing fiduciaries isn't just a legal task—it's a critical component of your comprehensive wealth plan. The people you select must be capable of managing the specific assets you’ve worked a lifetime to build.

At Endeavor Financial Group, our structured planning process helps you gain clarity on this. We start by analyzing the complexity of your financial life, considering factors such as:

- A diverse investment portfolio

- Multiple real estate holdings

- A family business with succession considerations

Understanding these details creates a clear profile of the skills your fiduciary will need.

We facilitate the conversations necessary to make these important decisions, ensuring they align with your long-term goals. While we don't draft legal documents, we work collaboratively with your estate planning attorney.

Our role is to ensure your financial strategy and legal framework are perfectly in sync, giving your chosen fiduciaries a clear and workable roadmap to follow. This cohesive approach helps prevent the gaps that can emerge when financial and legal plans are developed in isolation.

Frequently Asked Questions

How much does an estate fiduciary get paid?

Compensation varies by state and the complexity of the estate. Family members sometimes serve for free, while professional fiduciaries charge a fee. This is often a state-regulated percentage of the estate's value (e.g., 1-4%) or an hourly rate.

Can a fiduciary also be a beneficiary of the estate?

Yes, it's common for a beneficiary, like an adult child, to also serve as executor. They are legally required to treat all beneficiaries (including themselves) fairly and follow the terms of the will or trust precisely.

What is the difference between an executor and a trustee?

An executor’s role is generally short-term, focused on settling a will and distributing assets through the probate process. A trustee's role can last for many years, focused on the long-term management of assets held in a trust.

Can I appoint more than one person as co-fiduciaries?

Yes, but it can cause delays if they disagree on decisions. While co-fiduciaries offer checks and balances, appointing a single person is often better for roles needing quick action, like a Health Care Agent.

What happens if the person I appoint can't serve?

It's crucial to name at least one or two successor (backup) fiduciaries in your documents. If your first choice is unable or unwilling to serve when the time comes, the named successor can step in seamlessly without needing court intervention.