Failing to plan proactively can lead to substantial wealth erosion. Consider that households in the top 1% of the income distribution faced an average federal tax rate of 30.0% in 2022, according to the Congressional Budget Office. This figure doesn't even account for state and local taxes.

This article outlines 10 essential, actionable tax planning strategies designed for HNWIs, business owners, and pre-retirees. These aren't loopholes; they are legitimate, forward-thinking methods to help you build and preserve your legacy.

Key Takeaways

- Proactive tax planning for HNWIs integrates retirement, investment, charitable, and estate planning strategies.

- Key tactics include maximizing tax-advantaged accounts, strategic charitable giving, and tax-loss harvesting.

- Business owners can leverage unique advantages through entity structuring and the Qualified Small Business Stock (QSBS) exclusion.

- A successful plan requires a holistic approach with a team of professionals, not just isolated tactics.

Why Proactive Tax Planning is Crucial for High-Net-Worth Individuals

Effective tax planning is far more than an annual exercise to save money on April 15th. It’s a critical, ongoing component of long-term wealth management. For affluent families and individuals, the goal isn't simply to lower one year's tax bill but to create a sustainable framework that supports financial growth for generations.

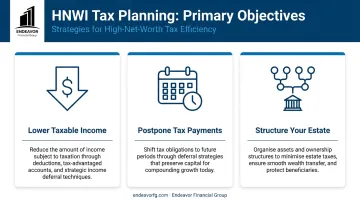

The primary objectives of strategic tax planning for HNWIs fall into three main categories:

- Lower your taxable income through legal deductions, credits, and deferral strategies.

- Postpone tax payments to a future date, allowing investments to grow unimpeded for longer.

- Structure your estate to minimize gift and estate taxes, ensuring a tax-efficient transfer of wealth.

Achieving these goals requires looking beyond basic deductions. The following 10 strategies are foundational to any comprehensive financial plan.

10 Key Tax Planning Strategies for High-Net-Worth Individuals

These strategies cover various aspects of your financial portfolio, from investments and retirement to charitable and estate goals. Each one is a powerful tool on its own, but they are most effective when used in concert.

1. Maximize Contributions to Tax-Advantaged Retirement Accounts

The most straightforward way to reduce your current taxable income is by contributing the maximum amount to tax-deferred accounts.

- 401(k)s and IRAs: For 2026, you can contribute up to $24,500 to a 401(k) and $7,500 to a traditional IRA.

- Catch-Up Contributions: If you are age 50 or over, you can contribute an additional $8,000 to your 401(k) and $1,100 to your IRA in 2026.

- Health Savings Accounts (HSAs): An HSA offers a triple tax advantage: tax-deductible contributions, tax-free growth, and tax-free withdrawals for qualified medical expenses. The 2026 contribution limits are $4,400 for individuals and $8,750 for families.

- For Business Owners: A SEP IRA or Solo 401(k) allows you to contribute significantly more—up to $72,000 in 2026—providing a substantial tool for reducing business income.

2. Implement Strategic Roth Conversions

A Roth conversion involves moving funds from a traditional (pre-tax) IRA or 401(k) to a Roth (after-tax) account. You pay ordinary income tax on the converted amount today in exchange for tax-free growth and, more importantly, tax-free withdrawals in retirement. For HNWIs, this can be a powerful hedge against potentially higher tax rates in the future.

The best time for a conversion is often during a lower-income year, such as after retiring but before taking Social Security, or during a year with significant business deductions.

3. Implement Tax-Loss Harvesting

Tax-loss harvesting is the practice of selling investments at a loss to offset capital gains taxes realized from selling other investments at a profit. If your losses exceed your gains, you can use up to $3,000 per year to offset ordinary income.

Be mindful of the wash-sale rule, which prohibits you from claiming a loss if you buy the same or a "substantially identical" security within 30 days before or after the sale. A financial advisor can help you navigate this rule by reinvesting the proceeds into a similar but distinct asset, maintaining your target portfolio allocation.

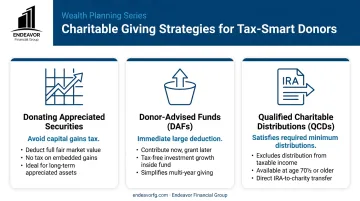

4. Use Advanced Charitable Giving Strategies

For charitably inclined HNWIs, there are more efficient ways to give than writing a check.

- Donating Appreciated Securities: Instead of selling a stock and donating the cash, you can donate the stock directly to a charity. This provides a double benefit: you avoid paying capital gains tax on the appreciation, and you can still deduct the full fair market value of the donation.

- Donor-Advised Funds (DAFs): A DAF allows you to "bunch" several years' worth of charitable contributions into a single year. You get a large, immediate tax deduction and can then recommend grants from the fund to your favorite charities over time.

- Qualified Charitable Distributions (QCDs): If you are over age 70½, you can donate up to $100,000 directly from your IRA to a charity. The distribution isn't counted as taxable income and can satisfy your Required Minimum Distribution (RMD).

5. Optimize Estate and Gift Tax Planning

Transferring wealth efficiently is a cornerstone of legacy planning.

The annual gift tax exclusion is a simple way to reduce the size of your taxable estate over time. In 2026, you can give up to $19,000 to as many individuals as you like without filing a gift tax return. A married couple can combine their exclusions to give up to $38,000 per recipient.

For larger transfers, irrevocable trusts like Spousal Lifetime Access Trusts (SLATs) or Grantor Retained Annuity Trusts (GRATs) can move significant assets out of your estate. This can help you use your lifetime gift and estate tax exemption (currently very high but scheduled to decrease) while potentially retaining some benefit or control.

6. Invest in Tax-Efficient Vehicles like Municipal Bonds

The interest income from municipal bonds ("munis") is typically exempt from federal income tax. If you buy bonds issued by your home state, the interest may also be exempt from state and local taxes.

For investors in high tax brackets, the tax-equivalent yield of a municipal bond can be much more attractive than that of a fully taxable corporate bond. They are often a core holding for the fixed-income portion of a portfolio.

7. Take Advantage of Real Estate Investment Tax Benefits

Direct ownership of investment real estate offers several unique tax advantages. You can deduct operating expenses, property taxes, and mortgage interest against rental income.

The most significant benefit is depreciation—a non-cash deduction that allows you to write off the cost of the property over time. This paper loss can shield rental income from taxes and sometimes even create a net loss that can offset other income, subject to certain limitations.

8. Optimize Business Structure and Deductions

For entrepreneurs, the right business structure is key. The choice between an S-corp, LLC, or C-corp has significant tax implications.

Additionally, owners of pass-through businesses may be eligible for the Qualified Business Income (QBI) deduction, which allows for a deduction of up to 20% of qualified business income. It’s also critical to work with a CPA to ensure you are maximizing all legitimate business expense deductions to lower your taxable profit.

9. Plan for the Qualified Small Business Stock (QSBS) Exclusion

The QSBS exclusion is one of the most generous provisions in the tax code for entrepreneurs and early-stage investors. If you hold stock in a qualifying small business for more than five years, you may be able to exclude 100% of the capital gains from federal tax upon sale.

The exclusion is generally capped at the greater of $10 million or 10 times your cost basis in the stock.

10. Manage and Time Stock Option Exercises

For executives with equity compensation, timing is everything.

With Incentive Stock Options (ISOs), exercising them typically does not trigger regular income tax at the time of exercise. However, it can trigger the Alternative Minimum Tax (AMT), so careful planning is required.

When you exercise Non-Qualified Stock Options (NSOs), the difference between the market price and your exercise price is taxed as ordinary income.

A well-timed exercise strategy can help manage the AMT impact and position you to qualify for more favorable long-term capital gains rates when you eventually sell the shares.

Putting It All Together: Implementing a Cohesive Tax Strategy

These ten strategies are powerful, but they aren’t standalone solutions. A Roth conversion can increase your income and phase you out of certain deductions, while a large charitable gift might change your cash flow needs for the year.

This is why a siloed approach—where your CPA, attorney, and financial advisor don't talk to each other—simply doesn't work.

A comprehensive financial planner acts as the "quarterback" for your financial team, ensuring all your professionals are working from the same playbook: yours.

At Endeavor Financial Group, we coordinate with your CPA and estate attorney to see the complete picture. This allows us to understand how a business succession decision impacts your taxes or how your portfolio aligns with your estate goals.

This holistic oversight is built on our five-step process, which moves from discovery and analysis to implementation and ongoing monitoring. It provides a clear roadmap, ensuring every financial decision aligns with your long-term objectives for financial freedom.

Conclusion

Strategic tax planning is not a one-time event; it's an ongoing process essential for preserving and growing the wealth you've worked so hard to build. Navigating these complex strategies requires professional guidance to avoid costly pitfalls and ensure every tactic aligns with your unique financial journey.

A proactive approach transforms tax strategy from a defensive obligation into a powerful tool for achieving your most important financial goals.

Ready to build a comprehensive, tax-efficient wealth plan tailored to your unique situation? Contact the team at Endeavor Financial Group today for a consultation.

Frequently Asked Questions

How do high-net-worth individuals plan their taxes?

They use a coordinated approach that combines retirement account maximization, strategic investments (like tax-loss harvesting and municipal bonds), advanced charitable giving, and sophisticated estate planning. This is typically guided by a team of professionals, including a financial advisor, CPA, and attorney.

Can I give my kids $100,000 tax-free?

You can give up to the annual gift tax exclusion amount ($18,000 for 2024) to any individual each year without tax consequences. A gift of $100,000 to one person would require you to file a gift tax return and use a portion of your lifetime gift tax exemption.

What is the difference between tax avoidance and tax evasion?

Tax avoidance is the legal use of strategies within the tax code to reduce your tax liability, such as the tactics discussed in this article. Tax evasion is the illegal, willful act of not paying taxes that are owed, for example, by underreporting income.

How often should I review my tax planning strategy?

Review your tax plan at least annually with your financial advisor. You should also revisit the plan after a significant life event like a marriage, inheritance, business sale, or major income change.

What is a donor-advised fund (DAF)?

A DAF is a charitable giving account you can establish at a public charity. You contribute assets to the fund, receive an immediate tax deduction, and then recommend grants from the fund to your chosen charities over time.

Are Roth IRA conversions always a good idea for high earners?

Not always. A conversion is most beneficial if you expect to be in a higher tax bracket in retirement. Since it triggers a large, immediate tax bill, the decision requires careful analysis of your current and projected future income.