That figure might not seem shocking at first, but it represents money that could have gone toward travel, hobbies, or simply providing a more comfortable financial cushion. It’s a slow drain on savings that can reduce your income, deplete your nest egg faster than planned, and limit your freedom.

Many of these taxes aren't fixed costs. They become expensive because of a lack of proactive planning. This article will break down how tax liabilities accumulate in retirement and provide actionable strategies to manage them, helping you keep more of your hard-earned money.

Key Takeaways

- Retirement tax liabilities often grow unexpectedly due to Required Minimum Distributions (RMDs), taxes on Social Security, and investment income.

- Your tax bill is driven by withdrawals from pre-tax accounts (401(k)s, Traditional IRAs), pensions, and capital gains.

- Key tax-reduction strategies include strategic Roth conversions, tax-efficient withdrawal sequencing, and using Qualified Charitable Distributions (QCDs).

- A proactive, holistic approach that integrates tax planning with your overall financial plan is crucial for maximizing your savings.

How Tax Liabilities for Retirees Typically Build Up

During your working years, you were in the accumulation phase, where your retirement savings grew tax-deferred. Retirement marks a fundamental shift to the distribution phase, where every withdrawal from a pre-tax account becomes taxable income. This change can catch many people by surprise.

This gradual tax impact can be deceptive. What begins with small, manageable withdrawals can escalate over time, eventually turning into a significant financial drain if left unplanned.

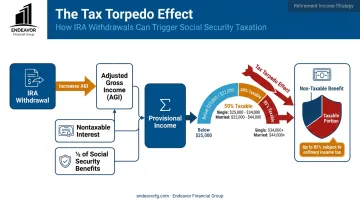

The "Tax Torpedo"

One of the biggest surprises for retirees is the "tax torpedo." This occurs when an increase in your income—often from an IRA withdrawal—causes a larger portion of your Social Security benefits to become taxable.

This interaction can create a sudden spike in your effective tax rate. In some cases, a single extra dollar of income can trigger taxes on an additional 85 cents of Social Security benefits.

The trigger for this is your provisional income, which is calculated as: Your Adjusted Gross Income (AGI) + Nontaxable Interest + One-half of your Social Security Benefits

If this total exceeds certain thresholds, up to 85% of your Social Security benefits can be taxed.

The RMD Effect

This problem is often compounded by Required Minimum Distributions (RMDs). The IRS requires you to start taking withdrawals from most retirement accounts beginning at age 73.

These forced withdrawals increase your taxable income, whether you need the money or not. A large RMD can easily push you into a higher tax bracket and right into the path of the tax torpedo, creating a costly cycle.

Key Drivers of Your Retirement Tax Bill

Managing your retirement tax bill starts with understanding your taxable income sources. It’s not just about how much you withdraw, but also about the type of account it comes from and the timing of the withdrawal.

Here are the primary sources of taxable income for most retirees:

- Withdrawals from Pre-Tax Retirement Accounts: Money you take from Traditional 401(k)s, 403(b)s, and Traditional IRAs is taxed as ordinary income. For decades, you received a tax deduction on these contributions, and now it’s time for the IRS to collect.

- Pension and Annuity Payments: Most payments from company pensions are fully or partially taxable as ordinary income. The specific tax treatment depends on whether you made any after-tax contributions to the plan.

- Investment Income: This includes earnings from your non-retirement brokerage accounts. These earnings are taxed based on two types of capital gains:

- Short-term gains: Profits from assets held for one year or less are taxed at your ordinary income tax rate.

- Long-term gains: Profits from assets held for more than one year are taxed at lower rates, typically 0%, 15%, or 20%, depending on your income.

- Social Security Benefits: Up to 85% of your benefits can become taxable if your provisional income exceeds certain thresholds. For a married couple filing jointly, this can start with an income as low as $32,000.

Tax-Reduction Strategies for Retirees

Effective tax reduction in retirement isn’t about a single loophole. It requires a multifaceted strategy covering decisions made before you retire, income management during retirement, and your broader financial life.

Strategies Based on Account Structure

1. Strategic Roth Conversions A Roth conversion involves moving funds from a Traditional IRA to a Roth IRA. You pay ordinary income tax on the converted amount today in exchange for tax-free withdrawals later.

The key is to convert funds strategically during low-income years—for example, after retiring but before Required Minimum Distributions (RMDs) and Social Security begin. This allows you to "fill up" lower tax brackets, paying taxes at a 12% or 22% rate now to avoid potentially higher rates.

2. Leverage Health Savings Accounts (HSAs) An HSA is one of the most powerful tax-advantaged accounts available. It offers a triple-tax advantage:

- Contributions are tax-deductible.

- The money grows tax-free.

- Withdrawals are tax-free when used for qualified medical expenses.

In retirement, an HSA can act as a tax-free slush fund for healthcare costs, which are often one of a retiree's largest expenses.

3. Use Smart Asset Location Asset location is the practice of placing different types of investments in the accounts that are best suited for them from a tax perspective.

- Tax-advantaged accounts (IRAs, 401(k)s): Hold tax-inefficient assets here, such as corporate bonds and REITs that generate ordinary income.

- Taxable brokerage accounts: This is the ideal place for tax-efficient assets like growth stocks and index funds you plan to hold for the long term to benefit from lower long-term capital gains rates.

Strategies for Managing Income and Assets

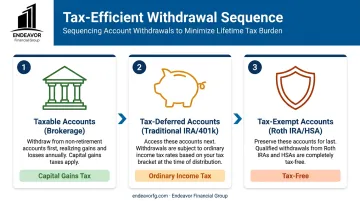

1. Implement a Tax-Efficient Withdrawal Sequence The order in which you tap your accounts can have a huge impact on your lifetime tax bill. The conventional wisdom is to withdraw funds in this order:

- Taxable Accounts: Tapping your brokerage account first allows your tax-deferred and tax-free accounts to continue growing. You’ll only pay capital gains tax on the appreciation, not the entire withdrawal.

- Tax-Deferred Accounts: Next, draw from your Traditional IRAs and 401(k)s.

- Tax-Exempt Accounts: Save your Roth IRAs and HSAs for last, as they provide tax-free income and can serve as a valuable hedge against future tax rate hikes.

2. Tax-Loss Harvesting If you have investments in a taxable brokerage account that have lost value, you can sell them to realize a loss. This loss can be used to offset capital gains elsewhere in your portfolio. If your losses exceed your gains, you can use up to $3,000 to offset your ordinary income each year. Just be mindful of the "wash sale" rule, which prevents you from claiming the loss if you buy a substantially identical security within 30 days before or after the sale.

Strategies That Leverage Your Broader Financial Picture

1. Use Qualified Charitable Distributions (QCDs) If you are age 70½ or older and charitably inclined, a Qualified Charitable Distribution (QCD) is an effective tool. It allows you to donate directly from your IRA to a qualified charity. For 2024, you can donate up to $105,000 this way. The donated amount is excluded from your adjusted gross income and can satisfy your RMD for the year, helping you avoid the associated income tax.

2. Strategic Gifting and Estate Planning Gifting assets to family members during your lifetime can be a way to reduce the size of your future taxable estate. For 2024, you can give up to $18,000 to any individual without having to file a gift tax return.

The Endeavor Advantage: A Strategic Approach to Tax Planning

Reducing taxes in retirement is not about a single trick. It’s about building a coordinated, long-term strategy that aligns with your overall financial goals. Effective tax management requires continuous adjustments for life events and changes in tax law—it’s not a "set it and forget it" task.

At Endeavor Financial Group, our comprehensive and consultative approach helps pre-retirees navigate these complexities. As fee-only fiduciaries, we are legally bound to act in your best interest, ensuring our recommendations are designed to optimize your financial situation, not to generate a commission.

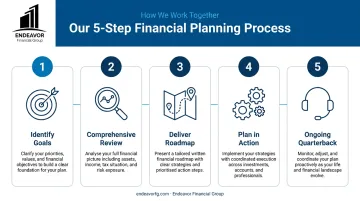

Our five-step process provides a clear roadmap for your financial future:

- We start by identifying your unique goals, priorities, and financial concerns.

- Our team conducts a comprehensive review of your finances to shape a preliminary strategy.

- We deliver a clear, actionable roadmap that includes a tax-efficient portfolio strategy tailored to your objectives.

- You'll have our full support as we work together to put your personalized plan into action.

- We serve as your ongoing financial quarterback, coordinating with other professionals and adapting your plan as your life evolves.

This integrated approach ensures tax planning is a core component of your financial strategy, not an afterthought.

Frequently Asked Questions

What is proactive tax planning for retirees?

It’s the process of strategically managing your income, investments, and withdrawals throughout the year to minimize your tax bill. This is different from reactive planning, which involves simply calculating what you owe at tax time.

What is the new $6,000 tax deduction for seniors?

This refers to the new enhanced deduction for seniors, effective for tax years 2025 through 2028. Individuals age 65 or older can claim an additional $6,000 deduction ($12,000 for a married couple if both qualify), though it phases out for higher-income taxpayers.

How can I reduce taxes on my Social Security benefits?

Taxes on Social Security are based on your "provisional income." The best way to reduce them is to carefully manage your other income sources, like IRA withdrawals, to keep your provisional income below the taxation thresholds.

Are Roth conversions a good idea for retirees?

Yes, they can be highly beneficial during the low-income years between retirement and the start of RMDs. The decision depends on your current versus expected future tax bracket, so it requires careful analysis.

What is a Required Minimum Distribution (RMD) and how is it taxed?

An RMD is the minimum amount you must withdraw annually from most retirement accounts, starting at age 73, as mandated by the IRS. This withdrawal is taxed as ordinary income in the year you take it.