For business owners, pre-retirees, and families who want their wealth to support loved ones for decades, a simple will isn't enough. You need a more robust strategy. Multi-generational estate planning is a comprehensive approach designed to transfer not only your assets but also your values, protecting your family’s future from taxes, external threats, and internal conflict.

This guide breaks down the entire process, from defining your family's core mission to implementing the right legal structures and avoiding the pitfalls that derail even the best-laid plans.

Key Takeaways

- Multi-generational planning is a long-term strategy for transferring both financial assets and family values to children, grandchildren, and beyond.

- The process involves defining a family mission, educating heirs, utilizing legal tools like trusts and LLCs, and establishing clear governance.

- Key goals are to minimize taxes, protect assets from creditors or divorce, and empower future generations to be responsible stewards of wealth.

- Common failures include poor communication, a lack of financial literacy in heirs, and having inadequate legal structures.

- Success requires a collaborative approach involving financial advisors, estate planning attorneys, and open family discussions.

What is Multi-Generational Estate Planning?

Multi-generational estate planning is the strategic process of structuring your financial and non-financial assets to be passed down effectively through two or more generations. The primary goal isn't just a one-time wealth transfer, but rather wealth preservation and the continuation of your family's legacy and values.

While traditional estate planning often stops with a simple will that distributes assets directly to your children, multi-generational planning takes a longer view.

It uses sophisticated, long-term structures like dynasty trusts to guide, protect, and grow that wealth for your grandchildren, great-grandchildren, and even future generations.

It’s the difference between giving a gift and building an endowment for your family’s future.

Why Multi-Generational Planning is Crucial for Your Family's Legacy

Multi-generational planning is more than a one-time inheritance—it’s a framework for creating a lasting family legacy. It provides structure and purpose for your wealth, ensuring it supports your descendants long after you’re gone.

This strategic approach delivers three crucial benefits: asset protection, tax efficiency, and the preservation of core family values.

Asset Protection

One of the greatest risks to inherited wealth is not market volatility, but life itself. A well-designed multi-generational plan shields assets from the personal and financial risks your heirs may face.

Long-term trusts can be structured with "spendthrift" provisions, which legally restrict a beneficiary’s ability to sell or give away their interest in the trust and prevent creditors from accessing trust assets. This means the wealth you leave behind is protected from potential future claims arising from lawsuits, business failures, or even a divorce.

Tax Minimization

Without proper planning, a significant portion of your estate can be lost to taxes. The federal estate tax rate can be as high as 40% on amounts exceeding the exemption threshold. Multi-generational planning uses specific strategies to minimize this impact over the long term.

Tools like dynasty trusts and strategic gifting are designed to significantly reduce estate, gift, and generation-skipping transfer (GST) taxes.

By placing assets in a trust that benefits multiple generations, for example, you can use your GST tax exemption to shelter that wealth from taxes for decades to come.

Preserving Family Values

Beyond the numbers, this type of planning is a powerful vehicle for instilling the principles that matter most to your family. It formalizes your vision for what the wealth should achieve, whether that’s funding education, encouraging entrepreneurship, or supporting philanthropic causes.

This is often captured in a family mission statement. This document articulates the purpose of the family's wealth, its core values, and the legacy it aims to create, serving as a guidepost for all future decisions.

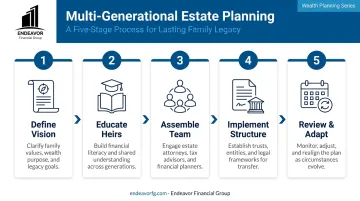

The 5-Step Process for Building Your Multi-Generational Estate Plan

Building a lasting legacy is a deliberate process that requires. It requires careful thought, open communication, and expert coordination. At Endeavor Financial Group, we guide families through a structured process that turns a broad vision into an actionable, resilient plan.

1. Define Your Family's Vision and Values

The first step is to answer the big question: Why? Before discussing trusts or tax strategies, your family needs to define the purpose of its wealth. This involves creating a family mission statement that articulates your shared values and the legacy you want to create. This foundational document will guide every subsequent decision.

2. Educate and Involve the Next Generation

The success of your plan depends on the people who will carry it out. Preparing your heirs is critical. Unfortunately, a recent Edward Jones study found that 35% of Americans do not plan to discuss wealth transfer with their families. This silence can lead to conflict and mismanagement.

Effective strategies for preparing the next generation include:

- Starting financial education early to build competence and confidence.

- Holding regular family meetings to discuss the family's wealth philosophy and goals.

- Involving them in philanthropic decisions to instill a sense of purpose and stewardship.

3. Assemble Your Professional Team

Multi-generational planning requires coordinated expertise from several professionals. As fee-only fiduciaries, we often act as the "quarterback" for our clients' financial teams, ensuring everyone is working from the same playbook.

Your team should include:

- A Certified Financial Planner (CFP®): To create the overarching financial strategy and ensure all pieces of the plan work together.

- An Estate Planning Attorney: To draft the necessary legal documents, such as wills and trusts.

- A Certified Public Accountant (CPA): To advise on tax implications and ensure the plan is as tax-efficient as possible.

4. Design and Implement the Legal and Financial Structure

This step translates your vision into a concrete legal and financial framework. Based on your family's goals, assets, and dynamics, your team will help you select and fund the appropriate tools. This could involve setting up long-term trusts, creating a family LLC for a business or real estate, or establishing a vehicle for charitable giving.

5. Conduct Regular Reviews and Adapt the Plan

A multi-generational plan is a living document that must adapt as circumstances change. Life changes, laws evolve, and family circumstances shift. We recommend reviewing your estate plan every 3-5 years, or immediately after any major life event.

These triggers include:

- A birth or death in the family

- Marriage or divorce

- A significant change in your financial situation

- The sale of a business

- Moving to a different state

Regular reviews ensure your plan remains aligned with your goals and compliant with current laws, giving you the flexibility to adapt as needed.

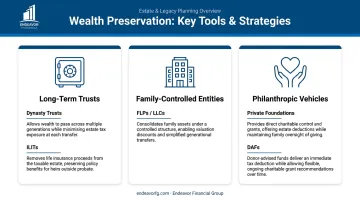

Key Tools and Strategies for Preserving Generational Wealth

A successful multi-generational plan relies on specific legal and financial instruments designed for longevity and protection. Here are some of the most common tools.

Long-Term Trusts

Trusts are the cornerstone of multi-generational planning, allowing you to set rules for how and when assets are distributed for decades.

- Dynasty Trusts: These powerful, long-term trusts are designed to pass wealth through multiple generations while minimizing estate and Generation-Skipping Transfer (GST) taxes. Depending on state law, they can last for many decades or even in perpetuity, sheltering assets from taxes and creditors for generations.

- Irrevocable Life Insurance Trusts (ILITs): An ILIT is a trust created to own a life insurance policy. By holding the policy outside of your taxable estate, the death benefit can be paid to your heirs free of estate taxes. This provides immediate, tax-free liquidity to cover estate taxes or other expenses, preventing your heirs from being forced to sell assets like a business or property.

Family-Controlled Entities

For families with a business or real estate portfolio, certain entities can help transfer wealth while maintaining control.

- Family Limited Partnerships (FLPs) and LLCs: These business structures allow senior family members to transfer ownership interests to younger generations over time, often at a discounted value for gift tax purposes. This strategy lets you move future appreciation out of your estate while retaining management control of the underlying assets.

Philanthropic Vehicles

Integrating philanthropy into your plan helps pass on family values and provides significant tax benefits.

- Private Foundations: A private foundation is a separate legal entity your family creates and controls to support charitable causes. It offers maximum control over grant-making and can be a powerful way to involve multiple generations in philanthropy.

- Donor-Advised Funds (DAFs): A DAF is a simpler alternative. You make a charitable contribution to a fund managed by a public charity, receive an immediate tax deduction, and then recommend grants to your favorite non-profits over time.

| Feature | Donor-Advised Fund (DAF) | Private Foundation |

|---|---|---|

| Control | You advise on grants; the sponsoring organization has legal control. | Your family or board has direct control over all decisions. |

| Administration | The sponsor handles all administrative tasks and filings. | The foundation is responsible for its own governance and tax filings. |

| Cost | Generally lower administrative costs and easier to set up. | Higher setup and ongoing administrative costs. |

| Anonymity | Grants can be made anonymously. | All grants and activities are a matter of public record. |

Common Pitfalls That Can Derail Your Family's Legacy (and How to Avoid Them)

Even the most technically sound plan can fail if it ignores the human element. Here are the most common mistakes and how to steer clear of them.

Lack of Communication

When heirs are left in the dark about the purpose of the wealth and their responsibilities, it can breed confusion, resentment, and conflict. This is a widespread problem—studies show only 25% of people receiving an inheritance felt prepared for the process.

To avoid this, implement regular family meetings to discuss the plan openly. A family mission statement can also help ensure everyone understands the "why" behind the wealth.

Unprepared Heirs

A significant inheritance can be a burden if the recipient lacks the financial literacy to manage it. This can lead to rapid depletion of assets and squandered opportunities.

The best approach is to start financial education early and make it an ongoing process. Involve younger family members in age-appropriate financial discussions to build their skills and confidence over time.

Inflexible Plan

A plan that is too rigid cannot adapt to changing tax laws, economic conditions, or evolving family needs. What works today may not work in twenty years.

Build flexibility directly into your legal documents. Tools like a "trust protector"—an independent third party who can modify the trust—or granting beneficiaries "powers of appointment" can allow the plan to evolve with your family.

Forgetting the "Human" Element

The biggest mistake is creating a plan that focuses solely on financial metrics while ignoring family dynamics, individual goals, and personal values. Wealth is a tool, not the end goal.

Instead, ensure the planning process is values-driven from the very beginning. The plan should empower each family member to pursue a fulfilling life, not just dictate financial outcomes.

Frequently Asked Questions

What are the best strategies for managing multi-generational wealth?

The best strategies combine tax-efficient legal structures, like dynasty trusts, with a strong focus on family governance and communication. Success depends on educating the next generation to be responsible stewards and maintaining a shared family vision.

Who is the best person to talk to about estate planning?

A coordinated team is essential. The process is often led by a comprehensive financial planner who acts as a "quarterback," working with an estate planning attorney for legal documents and a CPA for tax strategy.

How often should a multi-generational estate plan be reviewed?

You should review your plan every 3-5 years, or immediately after a major life event. This includes a birth, death, marriage, divorce, or a significant change in financial laws or your personal wealth.

What is the difference between a will and a long-term trust?

A will distributes assets after death and must go through the public probate process. In contrast, a long-term trust can manage assets for generations, bypasses probate for greater privacy, and offers far more control.

How can we prepare younger generations for their inheritance?

Start financial education early and make it practical. Involve them in family business discussions, let them participate in philanthropic decisions, and create opportunities for them to manage small amounts of money to build experience.

What role do family values play in estate planning?

Values are the foundation of a successful plan. They guide every decision, from how wealth should be used to what behaviors to encourage (like education or charity), ultimately defining what your family's legacy will be.