Navigating market volatility, rising inflation, and an uncertain tax landscape can feel overwhelming. According to Northwestern Mutual's 2024 study, 51% of U.S. adults cite inflation as the top obstacle to their financial security. This article will help you cut through the noise by outlining five clear signs that it’s time to partner with a professional financial advisor to build a confident retirement.

Key Takeaways

- A retirement financial advisor creates a comprehensive strategy covering investments, income, taxes, and your estate.

- Key signs you need an advisor include a complex financial situation, needing to convert savings into reliable income, or facing a major life transition.

- Look for a fiduciary with credentials like CFP®, who is legally obligated to act in your best interest.

- The cost of professional guidance is often far less than the expensive mistakes of a DIY approach, especially with significant assets at stake.

What is a Retirement Financial Advisor?

A retirement financial advisor is a professional who specializes in creating and managing a comprehensive financial strategy for life after work. This goes far beyond simple investment management; they take a holistic view, integrating everything from investments to tax strategies to ensure your finances work together efficiently.

Key Services a Retirement Advisor Provides

A qualified advisor manages the key financial aspects of retirement by offering several specialized services.

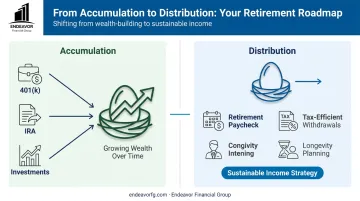

- Creates a reliable "paycheck" by structuring withdrawals from your various accounts (401(k), IRA, taxable brokerage).

- Aligns your investment portfolio with your retirement timeline, shifting from a growth focus to income and capital preservation.

- Minimizes your tax burden with strategic Roth conversions, tax-efficient withdrawal sequencing, and planning for Social Security taxes.

- Coordinates estate and long-term care planning to protect your assets and ensure they are passed on according to your wishes.

The Fiduciary Difference: Advisor vs. Planner

While "financial advisor" is a broad term, a Certified Financial Planner™ (CFP®) is a specific designation earned by professionals who meet rigorous education, examination, experience, and ethics requirements.

Most importantly, you should work with a fiduciary—someone legally and ethically required to act in your best interest at all times. This is non-negotiable for retirement planning, as it ensures the advice you receive is unbiased and tailored to your goals, not a salesperson's commission. The advisors at Endeavor Financial Group are proud to hold CFP® credentials and operate under this strict fiduciary standard.

5 Key Signs You Need a Financial Advisor for Retirement

Managing your own finances is achievable, but certain complexities and life stages signal the need for professional expertise. If you recognize yourself in any of the following situations, it might be time to seek guidance.

1. Your Financial Picture Has Become Too Complex

As you approach retirement, your financial life naturally becomes more complicated. You're likely managing multiple accounts accumulated over a long career—old 401(k)s, various IRAs, taxable brokerage accounts, and maybe even an HSA. Among adults ages 55 to 64, 70% have tax-preferred retirement savings accounts, and many have other assets to coordinate.

If you also own a business or have complex compensation like stock options, the challenge grows exponentially. A financial advisor can help you consolidate and coordinate these assets into a single, cohesive strategy, preventing inefficiencies and uncovering opportunities you might otherwise miss.

2. You're Unsure How to Turn Your Nest Egg into a Paycheck

Saving for retirement is one thing; spending those savings wisely is a completely different challenge. The transition from the accumulation phase to the distribution phase requires a clear, sustainable plan.

An advisor helps answer critical questions:

- How much can I safely withdraw each year?

- Which accounts should I draw from first to minimize taxes?

- How do I make sure my money lasts for 30+ years?

A professional can create a withdrawal strategy and stress-test it against market downturns and inflation. With Morningstar estimating a 3.7% starting safe withdrawal rate for 2024 and the Social Security Administration noting that about one in three 65-year-olds today will live to age 90, having a mathematically sound plan is essential.

3. You're Facing a Major Life Event Near Retirement

Major life events can have significant and lasting financial consequences, especially when they happen close to your retirement date. These situations require expert navigation to avoid costly mistakes.

Common examples include:

- Selling a business

- Receiving a significant inheritance

- Downsizing your home

- Navigating a divorce or the loss of a spouse

For instance, with the divorce rate for adults over 50 having doubled in recent decades, many face the challenge of splitting assets built over a lifetime. Similarly, Gallup reports that 74% of business owners plan to sell or transfer ownership as they approach retirement.

An advisor can provide the objective guidance needed to manage these transitions effectively.

4. You're Worried About Making Emotional Investment Decisions

It's human nature to feel fear during a market downturn or greed during a bull run. Unfortunately, acting on these emotions is one of the quickest ways to damage your retirement portfolio. Panic-selling during a correction or chasing risky returns can have devastating consequences when you're focused on capital preservation.

According to DALBAR's 2024 analysis, the average equity investor’s return significantly lagged the S&P 500, largely due to emotionally driven decisions. A financial advisor acts as a vital, objective buffer between your emotions and your money, providing the discipline needed to stick with a long-term strategy.

5. You Want to Optimize for Taxes and Your Estate

Successful retirement planning isn't just about how much money you have—it's about how much you get to keep. Without a smart tax strategy, you could lose a significant portion of your hard-earned savings to the IRS.

An advisor helps with advanced strategies that DIY planners often overlook, such as:

- Timing Roth conversions to take advantage of low-income years.

- Creating a tax-efficient withdrawal sequence from different account types.

- Planning for Required Minimum Distributions (RMDs), which begin at age 73.

- Structuring your estate to pass wealth to the next generation efficiently.

This level of optimization can add substantial value over the course of your retirement, ensuring your legacy is preserved according to your wishes.

How Endeavor Financial Group Can Help

If these signs resonate with you, know that you don't have to handle retirement planning on your own. Endeavor Financial Group is a firm of fiduciary, CFP® professionals specializing in comprehensive retirement planning for pre-retirees, executives, and business owners here in Indiana.

Our five-step structured process provides the clear roadmap you need. We begin with discovery to understand your unique goals and end with ongoing support to ensure your plan adapts as your life changes. This disciplined approach is how we solve the challenges outlined above:

- We create a single, cohesive financial strategy, simplifying all your accounts into one clear plan.

- We build a sustainable, tax-efficient income plan to design a reliable retirement "paycheck."

- We provide steady guidance to help you make sound financial decisions during major life events.

- We act as your objective partner to help you avoid emotional investing mistakes and stay on track with your goals.

- We help you keep more of your money by optimizing your finances for taxes and estate planning.

Your Confident Retirement Awaits

The five signs discussed are strong indicators that professional guidance isn't a luxury but a necessity for achieving your retirement goals. The real objective is to retire with a plan that provides both financial security and genuine peace of mind.

If you recognize yourself in any of these situations, it's time to start a conversation. Take the first step toward building a clear financial roadmap by scheduling a complimentary consultation with our team at Endeavor Financial Group.

Frequently Asked Questions

Do I need a financial advisor for retirement?

An advisor is highly recommended if your finances are complex, you're nearing retirement and need an income strategy, or you want to optimize for taxes and estate planning. They provide a clear roadmap and objective guidance.

What is the biggest mistake most people make regarding retirement?

A common mistake is underestimating the future impact of inflation and healthcare costs. Another is failing to create a tax-efficient withdrawal strategy, which can needlessly deplete savings over time.

How much do I need to retire on $80,000 a year at 60?

There's no single number, as it depends on your other income sources, lifestyle, health, and tax situation. An advisor uses comprehensive planning software to calculate a personalized and reliable figure based on your unique circumstances.

What's the difference between a financial advisor and a financial planner?

"Advisor" is a general term. A "planner," especially a Certified Financial Planner™ (CFP®), engages in a holistic planning process covering all aspects of your financial life and often has a legally binding fiduciary duty.

Are financial advisors only for the wealthy?

This is a common myth. According to a 2024 survey from the CFP Board, 42% of CFP® professionals do not require clients to have a minimum of investable assets. This guidance helps prevent costly mistakes, making it valuable for anyone building retirement savings.

What does it mean if an advisor is a fiduciary?

A fiduciary is a professional legally and ethically required to act in their client's best interest. This means they must avoid conflicts of interest, putting your financial goals ahead of their own compensation or incentives.