That gap is expensive. A rushed or absent succession plan doesn't just threaten the business — it threatens the jobs of everyone who depends on it, and the financial future of the owner who built it.

Business succession planning, in plain terms, is a formal strategy for transitioning ownership and leadership in a way that protects what you've built. It answers three questions: Who takes over? How does the transition happen? And what does the owner walk away with?

This guide covers the most practical succession options, a step-by-step planning process, the financial considerations that most owners underestimate, and the most common mistakes to avoid before it's too late.

Key Takeaways

- Start succession planning 3–5 years before any planned transition — earlier is better

- There are multiple exit paths (family transfer, management buyout, ESOP, third-party sale) and your goals determine which fits

- A formal plan protects business value, preserves employee jobs, and ties directly to your retirement income security

- Build a coordinated advisor team — financial planner, CPA, and attorney — early in the process

- Delaying the process is the most common reason owners leave money — and options — on the table

Why Most Small Businesses Aren't Prepared

The numbers are stark. Gallup reported in 2025 that 52.3% of U.S. employer businesses are owned by people 55 or older — roughly 3 million firms approaching a natural transition window. Yet formal planning lags far behind that demographic reality.

Three reasons consistently explain the delay:

- Emotional resistance — For most founders, the business is bound up in their identity. Planning for an exit forces an uncomfortable reckoning that many owners simply postpone

- Uncertainty about where to start — The process involves legal, tax, financial, and operational dimensions simultaneously, and the complexity can feel paralyzing

- The "not yet" mindset — Many owners assume succession planning is a retirement-year task, not something that requires a 3–5 year runway

The consequences of delay are real. Family business survival statistics illustrate the risk: roughly 30% of family businesses transition successfully to the second generation, and only about 12–13% reach the third — a figure that includes businesses sold or merged, not only those that failed. Even so, unplanned transitions increase vulnerability significantly.

Nearly half of all business exits are forced by unexpected events — death, disability, or sudden financial distress — not voluntary retirement. Without a plan in place, a sudden leadership change can destabilize operations, strain customer relationships, and materially reduce what the business is worth.

Your Succession Options: Which Path Is Right for You?

There's no universal answer here. The right exit path depends on your personal goals, your timeline, the financial health of the business, and whether a qualified successor already exists. Broadly, options fall into two categories.

Internal Succession

Family ownership transfer passes leadership and ownership to the next generation. When estate planning is integrated from the start, it preserves the business legacy and keeps value within the family. Without it, tax exposure and family conflict can unravel years of work.

A will or trust must align with the succession plan, and gifting strategies or family limited partnerships may play a role depending on the estate's size.

Management buyout or employee succession involves a trusted leadership team or key employee purchasing the business. This often requires a structured buy-sell agreement and may involve seller financing (where the owner acts as the lender) or an SBA-backed loan to fund the purchase. The main challenge is financial — most employees don't have the capital on hand — so the deal structure often determines whether the transition succeeds.

Employee Stock Ownership Plans (ESOPs) allow employees to gradually acquire ownership through a company-funded retirement trust. For eligible C corporation sellers, Section 1042 of the tax code allows capital gains deferral if the ESOP owns at least 30% of company value after the sale and stock was held for at least three years. The NCEO reports 6,609 ESOP plans in the U.S. as of 2023, covering more than 15 million participants — a legitimate but specialized path that requires experienced legal and financial advisors to structure correctly.

External Succession

A third-party sale means selling to a strategic buyer (a competitor or company that values your market position) or a financial buyer (private equity or a family office). This path typically commands the highest price — but also demands the most preparation.

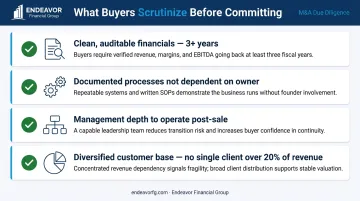

Buyers scrutinize every aspect of the business before committing, including:

- Clean, auditable financials for at least 3 years

- Documented processes that don't depend on the owner

- Management depth that can operate post-sale

- A diversified customer base (no single client >20% of revenue)

Owner-dependent businesses with concentrated customer bases are harder to sell and command lower multiples. BizBuySell notes that sellers often set asking prices 10–15% above true valuation, so knowing your actual market value before entering negotiations is essential.

What Are the 5 Steps of Succession Planning?

This framework works regardless of how far out your transition is. The earlier you start, the more options you preserve.

Step 1: Document Your Organizational Structure and Future Goals

Map the current org chart, then project what the business needs to look like without you running it. This step surfaces the gap between where the business is today and where it needs to be to operate independently. Many owners discover at this stage that the business is more owner-dependent than they realized — a problem that takes years to fix.

Step 2: Identify Key Roles and Define What Success Looks Like

Not every role needs a succession plan. Focus on positions that are critical to operations and revenue. For each one, define the required skills, knowledge, and decision-making authority so that candidates can be evaluated against a concrete standard rather than a vague impression.

Step 3: Identify and Develop Potential Successors

This step requires actual conversations, not assumptions. In family businesses especially, owners often assume a child or sibling wants to take over without ever asking directly. That assumption is dangerous.

Meet with high-potential employees or family members individually. Gauge their interest, assess their readiness, and understand their goals. The successor you expect may not want the role; the one you overlooked might be the right fit.

Endeavor Financial Group's advisors regularly help facilitate these conversations with business owners, providing the objective perspective that's hard to maintain when family dynamics or long-standing employee relationships are involved.

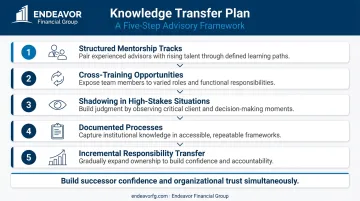

Step 4: Create a Knowledge Transfer and Leadership Development Plan

Institutional knowledge doesn't transfer automatically. Customer relationships, supplier terms, internal processes, and operational judgment accumulate over years and live in the owner's head. This step involves:

- Structured mentorship tracks pairing the owner with the successor

- Cross-training opportunities across functions

- Shadowing in high-stakes situations (client negotiations, vendor discussions, key decisions)

- Documented processes that capture how the business actually runs

- Incremental responsibility transfer — giving the successor real ownership of decisions before the formal handover

The goal is to build the successor's confidence and the organization's confidence in them simultaneously.

Step 5: Review, Monitor, and Update the Plan Regularly

A succession plan filed away and forgotten won't hold up when you need it. Circumstances change: key people leave, valuations shift, tax laws evolve, and personal situations change. Schedule annual reviews as a standing priority, and trigger an immediate review after major events — a key employee departure, a significant change in business performance, or a new tax law.

Endeavor Financial Group builds this review cadence directly into its ongoing advisory process, treating the succession plan as a living component of the client's overall financial strategy.

The Financial and Personal Side of Succession Planning

For most small business owners, the business represents the majority of personal net worth — some estimates put it at 80% or more of total wealth. That means succession planning isn't just a business exercise. It's a personal financial event, and it requires its own dedicated planning.

Business Valuation: Know What You're Working With

Get a formal valuation from a certified professional before doing anything else. Many owners significantly over- or underestimate what their business is actually worth, and a gap between expectation and reality is one of the most common reasons transitions stall or fall apart entirely.

A professional valuation does more than produce a number. It identifies the operational factors — customer concentration, management depth, earnings quality, documented processes — that drive value up or suppress it. That gives you a roadmap for improvements you can make before the transition, when there's still time to act on them.

Tax, Estate, and Legal Structure

How a succession is structured dramatically affects what the owner actually keeps. Key decisions include:

- Asset sale vs. stock sale — different tax treatment for buyer and seller, with meaningful implications for net proceeds

- Buy-sell agreements — legally binding documents that govern how ownership changes hands

- Entity structure — whether the business is structured as an S corp, C corp, LLC, or partnership affects available succession strategies

- Gifting and trust strategies — the federal estate tax basic exclusion is $13.99 million in 2025, with an annual gift tax exclusion of $19,000 per recipient. These figures are scheduled to change after 2025 under current law, which makes modeling these scenarios now — before those options narrow — particularly important

These decisions need to be modeled with a CPA and estate attorney 2–3 years before a planned transition, when the most options are still open. The same window matters for personal financial planning — because once the transaction closes, many of those levers disappear.

Planning Your Own Financial Future Post-Transition

The sale or transfer of a business is a liquidity event. Done well, it funds decades of financial security. Without a clear plan, the proceeds can expose you to unnecessary tax liability and investment drift — quietly eroding wealth you spent a career building.

This is where many business owners arrive underprepared. They focus intensely on the transaction itself and underinvest in what comes after. The proceeds need to be aligned with retirement income needs, investment objectives, and legacy goals through a coordinated financial plan.

Endeavor Financial Group's CFP® professionals work specifically with small business owners and pre-retirees to do exactly this — connect the business transition to a long-term personal financial strategy. Their five-step process, running from discovery and analysis through implementation and ongoing monitoring, treats the succession outcome and the retirement plan as one integrated picture.

Common Pitfalls to Avoid

Most succession plans don't fail because of bad intentions — they fail because of avoidable mistakes. Three patterns show up repeatedly:

Starting Too Late

Rushed timelines suppress options, reduce valuation leverage, and force reactive decisions. The 3–5 year preparation window isn't arbitrary — it's the minimum time needed to address valuation gaps, develop successors, and structure the transition tax-efficiently.

Overlooking the Human Side

Succession involves people, not just paperwork. Employees worry about job security. Customers worry about continuity. According to MassMutual's 2022 Business Owner Perspectives Study, about 25% of chosen successors are unaware they've been selected — a communication failure that creates real risk. A solid plan addresses stakeholder communication proactively, not as an afterthought.

Relying on a Single Advisor

Many owners talk only to their attorney or only to their accountant. Both bring critical expertise, but neither sees the complete picture. Effective succession planning requires coordinated input from legal, tax, financial, and banking professionals — working together, not in silos.

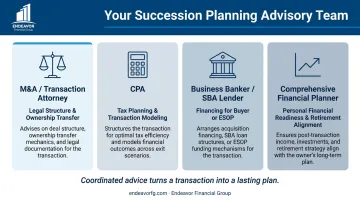

Building the Right Team of Advisors

The earlier you assemble this team, the better. Time is the resource that makes every other decision easier.

| Advisor | Primary Role in Succession |

|---|---|

| M&A / Transaction Attorney | Legal structure, buy-sell agreements, ownership transfer documentation |

| CPA | Tax planning, entity structure, transaction modeling, estate coordination |

| Business Banker / SBA Lender | Financing options for buyer, ESOP, or management buyout |

| Comprehensive Financial Planner | Personal financial readiness, liquidity event management, retirement income alignment |

Research consistently shows that owners without a formal advisory team are far more likely to stall in early planning stages. A 2013 Exit Planning Institute survey found only 14% of owners had established a coordinated transition team — most relied on one or two relationships and hoped that was enough.

Endeavor Financial Group works alongside attorneys, CPAs, and lenders to make sure the succession plan holds up on the personal side of the ledger. While other advisors focus on legal structures and tax outcomes, Endeavor's role is to ensure the transition actually supports the owner's financial life: retirement income, investment strategy, estate intentions, and long-term security. That kind of cross-functional coordination is what turns a signed transaction into a plan that works.

Frequently Asked Questions

What are the 5 steps of succession planning?

The five core steps are: (1) document your organizational structure and goals, (2) identify key roles and define success criteria, (3) identify and develop potential successors, (4) create a knowledge transfer and leadership development plan, and (5) review and update the plan regularly. Each step builds on the last — start well before any planned transition to keep your options open.

What are the 4 C's of family business?

The four C's are Continuity, Culture, Capital, and Communication. Together, they cover keeping the business operational across generations, preserving its identity, managing ownership and finances equitably, and keeping communication open among family members and stakeholders throughout the transition.

When should a small business owner start succession planning?

At least 3–5 years before any planned transition. Starting early preserves the most options — for tax structuring, successor development, valuation improvement, and deal structure. Owners who wait until they're ready to exit often find that their best choices have already closed.

What is the difference between succession planning and an exit strategy?

Succession planning focuses on who takes over and how leadership and ownership transfer. An exit strategy is the broader financial and operational framework for how the owner leaves the business. The two overlap significantly and are most effective when planned together rather than treated as separate processes.

How do I determine the value of my business for succession planning?

Work with a certified business valuator or M&A advisor for a formal appraisal. A credible valuation accounts for earnings quality, customer concentration, management depth, and comparable market transactions, giving you a baseline to improve from before the transition begins.

What role does a financial advisor play in business succession planning?

A financial advisor connects the business transition to the owner's personal financial goals — managing the liquidity event from a sale, aligning proceeds with retirement income needs, and ensuring long-term financial security beyond the business. They also coordinate with the legal and tax professionals on the team to make sure every piece of the plan works together.