You're not alone if you find it confusing. A comprehensive 2022 survey from Morgan Stanley found that only 39% of stock plan participants feel they understand how taxes will impact their benefits. This knowledge gap can lead to costly mistakes and missed opportunities.

This guide is designed to change that. We'll break down the different types of equity, explain exactly when and how they are taxed, and provide clear strategies to help you maximize your after-tax returns.

TL;DR: Your Equity Compensation Tax Cheat Sheet

- Equity compensation is taxed at different stages: vesting (RSUs), exercise (stock options), and sale (all types).

- The three main types are Restricted Stock Units (RSUs), Incentive Stock Options (ISOs), and Non-Qualified Stock Options (NSOs), each with unique tax rules.

- You'll face either ordinary income tax or capital gains tax (short-term or long-term), depending on the equity type and how long you hold the shares.

- Proactive tax planning, such as timing your sales and holding shares for over a year, can significantly reduce your tax burden.

Understanding the Main Types of Equity Compensation

Building an effective tax strategy starts with understanding the type of equity you have. Most compensation plans revolve around three common types.

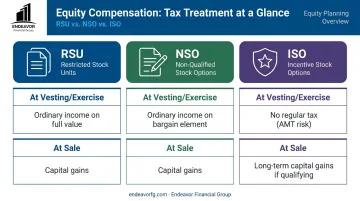

Restricted Stock Units (RSUs)

RSUs are a straightforward grant of company shares that you receive after meeting certain conditions, known as a vesting schedule. This schedule is typically time-based (for example, 25% of your shares vest each year for four years). Unlike options, you don't purchase RSUs; they are granted to you and have immediate value as soon as they vest.

Incentive Stock Options (ISOs)

ISOs give you the right to purchase company stock at a predetermined price, often called the "strike price" or "exercise price." The main appeal is their potential for preferential tax treatment. If you meet specific holding period rules, the gain can be taxed at lower long-term capital gains rates.

However, ISOs come with complex rules, including the potential to trigger the Alternative Minimum Tax (AMT).

Non-Qualified Stock Options (NSOs or NQSOs)

NSOs are another type of stock option that gives you the right to buy company shares at a set strike price. They are more flexible than ISOs and don't have the same strict holding period requirements. The trade-off is that they don't qualify for the same special tax treatment. When you exercise NSOs, the difference between the strike price and the stock's current market value is taxed as ordinary income.

The Three Key Taxable Events in Your Equity's Lifecycle

Understanding when you are taxed is just as important as knowing how. Your equity journey has three critical milestones, but a tax bill isn't triggered at every step.

Grant Date: This is the day your company officially promises you the equity. For all three types (RSUs, ISOs, and NSOs), the grant date is typically not a taxable event. It’s simply the start of the clock on your vesting or holding periods.

Vesting/Exercise Date: This is often the first major taxable event, triggered when you gain control or ownership of the shares.

- For RSUs, this happens when your shares vest.

- For stock options (ISOs/NSOs), this occurs when you exercise your right to buy the shares.

Sale Date: This is the day you sell your shares. This event almost always triggers a tax liability, requiring you to report either a capital gain or a capital loss.

A Deeper Dive: How Each Equity Type Is Taxed

Each type of equity compensation has a different tax timeline. Let's break down how the IRS treats each one at key taxable events.

Tax Treatment of RSUs

RSUs are the simplest to understand from a tax perspective.

At Vesting: The moment your RSUs vest, the total market value of the shares is considered ordinary income and is subject to federal, state, and payroll (Social Security and Medicare) taxes. Your employer will typically withhold a portion of the shares to cover these taxes.

- Example: 100 RSUs vest when the stock price is $50 per share. You will have $5,000 of taxable ordinary income for that year ($100 x $50).

At Sale: When you later sell the shares, any profit you make is taxed as a capital gain. Your cost basis is the market value of the shares on the day they vested.

- Held less than one year: If you sell within a year of vesting, the gain is a short-term capital gain, taxed at your ordinary income rate.

- Held more than one year: If you hold the shares for over a year after vesting, the gain is a long-term capital gain, taxed at more favorable rates (0%, 15%, or 20%).

Tax Treatment of NSOs

NSOs are taxed at both exercise and sale, but in different ways.

At Exercise: When you exercise your NSOs, the "bargain element"—the difference between the market price and your lower strike price—is taxed as ordinary income.

- Example: You exercise 100 NSOs with a strike price of $10 when the market price is $60. The bargain element is $50 per share ($60 - $10). You will have $5,000 of taxable ordinary income (100 shares x $50).

At Sale: Your cost basis for the shares is the market value on the exercise date ($60 in our example). Any gain above that price when you sell is a short-term or long-term capital gain, following the same one-year holding rule as RSUs.

Tax Treatment of ISOs

ISOs offer the most potential tax advantages but also come with the most complicated rules.

- At Exercise: The primary tax benefit is that no regular income tax is due when you exercise ISOs.

However, the bargain element is considered an "add-back" for the Alternative Minimum Tax (AMT). A large ISO exercise can trigger this separate tax, creating a significant liability even if you don't sell any shares.

At Sale (Qualifying Disposition): To get the best tax treatment, you must meet two holding period requirements:

- Sell the shares more than two years after the grant date.

- Sell the shares more than one year after the exercise date.

If you meet both, the entire gain from your strike price to your sale price is taxed as a long-term capital gain. Unlike NSOs, this allows the entire gain to be taxed at more favorable long-term capital gains rates.

At Sale (Disqualifying Disposition): If you fail to meet either of the holding period rules, the tax benefits are lost. The bargain element at the time of exercise is taxed as ordinary income, and any additional gain is treated as a short-term or long-term capital gain, depending on how long you held the shares after exercise.

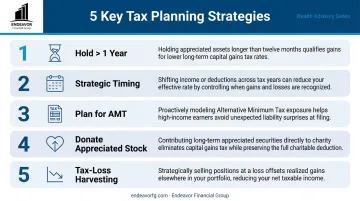

5 Key Strategies for Tax-Efficient Equity Planning

Managing your equity isn't passive. Making strategic decisions about when to exercise, hold, or sell can save you thousands of dollars in taxes.

Hold Shares for More Than a Year This is the most fundamental strategy. The difference between short-term and long-term capital gains tax rates is significant. For tax year 2026, short-term gains are taxed as ordinary income at rates up to 37%, while long-term gains are taxed at much lower rates of 0%, 15%, or 20%.

Holding your vested RSU or exercised option shares for at least one year and a day can dramatically increase your after-tax return, depending on your total taxable income.

Time Your Exercise and Sale Strategically Because the value of your vested RSUs or exercised options adds to your ordinary income, it can push you into a higher tax bracket. If possible, consider timing these events for a year when your other income might be lower. For example, if you plan to take a sabbatical, change jobs, or anticipate a lower bonus, that could be an opportune year to realize equity-related income.

Plan for the Alternative Minimum Tax (AMT) For Incentive Stock Option (ISO) holders, this is non-negotiable. The Alternative Minimum Tax (AMT) is a parallel tax system, and exercising a large number of ISOs can trigger it unexpectedly.

Before you exercise, it's critical to run a tax projection to see how many shares you can exercise without triggering the AMT. Spreading exercises over multiple tax years is a smart way to manage this liability.

Donate Appreciated Stock to Charity If you are charitably inclined, donating shares you've held for more than a year is one of the most tax-efficient giving strategies. By donating the stock directly to a qualified charity, you can generally achieve two powerful benefits:

- You may be able to deduct the full fair market value of the stock.

- You avoid paying any capital gains tax on the appreciation.

Use Tax-Loss Harvesting If you have other investments in a taxable brokerage account, you can use tax-loss harvesting to offset gains from your company stock. This involves selling other investments that are at a loss to cancel out your capital gains.

If your losses exceed your gains, you can use up to $3,000 to offset your ordinary income each year and carry forward the rest to future years.

Bringing It All Together: Why a Holistic Financial Plan is Crucial

Managing equity compensation taxes shouldn't happen in a vacuum. A decision about when to sell your RSUs could impact your retirement savings goals, and an ISO exercise strategy must account for your overall cash flow. This is where a holistic financial plan becomes essential.

A significant risk for many executives and employees is being over-concentrated in a single stock. While you believe in your company's future, having too much of your net worth tied to one asset is a high-stakes gamble. A comprehensive financial plan helps you build a disciplined diversification strategy that aligns with your risk tolerance and long-term goals.

At Endeavor Financial Group, our consultative process brings clarity to these complex situations. As fee-only fiduciaries, we are legally bound to act in your best interest.

Our approach involves:

- Understanding your unique goals and complete financial picture.

- Building a personalized roadmap that integrates your equity awards.

- Coordinating with your tax and legal professionals for a cohesive strategy.

This ensures every decision, from exercising options to diversifying your portfolio, supports your journey toward financial freedom.

Frequently Asked Questions

What is equity compensation planning?

It's the process of strategically managing your stock awards to maximize their value while minimizing tax liability. This involves aligning decisions about your equity with your broader financial goals, such as retirement, diversification, and estate planning.

What are the types of equity compensation?

The most common types are Restricted Stock Units (RSUs), which are outright grants of stock; Incentive Stock Options (ISOs), which are tax-advantaged options; and Non-Qualified Stock Options (NSOs), which are more flexible stock options.

Which is better: ISOs or RSUs?

Neither is universally "better." ISOs offer greater tax advantages but are more complex (e.g., AMT risk), while RSUs are simpler and provide immediate value at vesting. The right choice depends on your financial situation and risk tolerance.

How is equity compensation taxed?

It's typically taxed as ordinary income when you receive control of the value (at vesting for RSUs, at exercise for NSOs). The shares are then taxed as a capital gain (either short- or long-term) when you sell them.