Achieving major milestones like a comfortable retirement or a smooth business succession depends on a strategy that properly balances risk and reward. Generic models simply can't account for your specific needs. This guide will walk you through the core principles of asset allocation and show you how to build a portfolio that aligns with your personal goals, timeline, and risk tolerance.

Key Takeaways

- Your ideal mix depends on your personal goals, time horizon, and risk tolerance.

- Stocks offer growth, bonds provide stability, and cash ensures liquidity.

- Rebalance your portfolio regularly to maintain your target allocation.

- A fiduciary advisor can help build a personalized strategy aligned with your goals.

What is Asset Allocation?

Asset allocation is an investment strategy that aims to balance risk and reward by apportioning a portfolio's assets according to an individual's goals, risk tolerance, and investment horizon.

This strategy follows the simple principle of not putting all your eggs in one basket. Different asset classes perform differently under various market conditions—when stocks are struggling, for instance, bonds often provide stability.

In fact, a Vanguard study found that asset allocation drives about 88% of a portfolio's long-term performance, making it the most critical investment decision you can make.

Core Asset Classes Explained

- Stocks (Equities): These are the engine for long-term growth. They represent ownership in a company and have the highest potential for returns over time, though they also come with higher volatility. Diversifying within this class might mean holding a mix of large-cap (large companies), small-cap (smaller companies), domestic, and international stocks.

- Bonds (Fixed Income): Bonds provide income and stability. When you buy a bond, you are essentially lending money to a government or corporation in exchange for regular interest payments. They generally carry less risk than stocks and can act as a valuable counterbalance during stock market downturns.

- Cash and Cash Equivalents: This is your portfolio's safety net. It includes things like savings accounts and money market funds. The goal here isn't growth, but capital preservation and liquidity for short-term needs or emergencies.

- Alternative Investments: This broad category includes assets like real estate, commodities (like gold), or private equity. Alternatives can offer further diversification because they often move independently of traditional stock and bond markets, but they can also come with unique risks and complexities.

Benefits of a Proper Asset Allocation Strategy

- Risk Management: By spreading investments across assets that don't move in perfect sync, you can cushion your portfolio against a severe downturn in any single sector.

- Optimized Returns: The goal isn't just to avoid risk, but to create a blend of assets positioned to meet or exceed your return targets over the long term.

- Financial Discipline: Having a clear strategy helps you avoid making emotional, reactive decisions—like selling in a panic or chasing hot trends—during periods of market volatility.

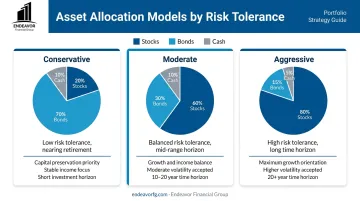

Key Factors for Customizing Your Asset Allocation

The "right" asset allocation isn't universal; it's deeply personal. Your ideal mix depends on a thorough evaluation of several factors unique to your situation.

Factor 1: Financial Goals

Your goals dictate the strategy. Are you saving for retirement in 20 years, a down payment on a house in five years, or your child's college education in 10? Each goal requires a different approach.

For instance, a long-term retirement fund can handle the ups and downs of a more aggressive, stock-heavy portfolio. But a short-term goal like a house down payment requires a conservative, capital-preservation approach focused on bonds and cash to ensure the money is there when you need it.

Factor 2: Time Horizon

The amount of time you have to invest directly impacts how much risk you can afford to take. A longer time horizon gives your portfolio more time to recover from potential market downturns. This makes a higher allocation to growth-oriented assets like stocks more suitable for a 30-year-old than for someone five years from retirement.

Factor 3: Risk Tolerance

This is about more than just numbers; it's about your emotional and financial ability to withstand market swings. You need to be honest with yourself: how would you react if your portfolio dropped 20% in a few months?

Your asset allocation should let you sleep at night. A strategy that is too aggressive for your comfort level might cause you to sell at the worst possible time.

Factor 4: Liquidity Needs

It's crucial to consider how much cash you need on hand for emergencies or planned short-term expenses. This prevents you from being forced to sell long-term investments at an inopportune moment to cover an unexpected bill. A 2024 Federal Reserve report found that only 63% of adults could cover a hypothetical $400 emergency expense using cash or its equivalent. This statistic underscores the need for a liquid cash reserve.

Factor 5: Tax Situation

A smart asset allocation strategy is also a tax-efficient one. This concept, often called "asset location," involves placing different types of investments in the most appropriate accounts. For example, tax-inefficient assets like high-yield bonds might be better held in tax-advantaged accounts (like a 401(k) or IRA), while more tax-efficient assets like broad-market index funds can be held in taxable brokerage accounts.

Factor 6: Personal Values (ESG)

A growing number of investors want to align their portfolios with their personal values. This can involve focusing on companies that meet certain Environmental, Social, and Governance (ESG) criteria. If sustainable or socially responsible investing is important to you, this can be another layer of customization in your portfolio.

The Critical Role of Rebalancing in Your Custom Portfolio

Building your custom portfolio is the first step; maintaining it is the key to long-term success. This is done through rebalancing—the process of periodically buying or selling assets to return to your original target allocation.

Over time, market movements will cause your portfolio to "drift." If stocks have a strong year, your intended 60% stock allocation might grow to 70%. While portfolio growth is positive, this drift also means your portfolio is now riskier than you originally intended. Rebalancing is a disciplined way to "sell high and buy low" by trimming the outperforming assets and adding to the underperforming ones.

You can rebalance based on a set schedule (e.g., quarterly or annually) or whenever an asset class deviates from its target by a specific threshold, such as 5%.

According to Vanguard research, for most diversified portfolios, annual or semiannual monitoring with rebalancing at 5% thresholds is an effective way to balance risk control and costs. This discipline is a key part of long-term investment success.

How Endeavor Financial Group Crafts Your Personalized Investment Strategy

While the principles of asset allocation are straightforward, implementing and managing a customized strategy requires expertise—especially for those with complex financial lives, like business owners or pre-retirees. This is where a professional, consultative approach is essential.

At Endeavor Financial Group, we go beyond simple asset management to create a holistic financial plan. We use a structured, five-step process to build and maintain a custom asset allocation strategy that evolves with your life.

- Discovery: We start by getting to know you, your financial goals, and your values to ensure our partnership is a good fit from day one.

- Analysis: Our team takes a deep dive into your complete financial picture, gathering the information needed to shape a preliminary plan.

- Strategy Development: We deliver a comprehensive roadmap with your optimal asset mix, including strategic long-term allocations and tax-efficient tactical adjustments.

- Implementation: We put your plan into action, building a results-focused portfolio of individual investments such as stocks, bonds, and other assets.

- Monitoring & Adjusting: As your life and goals evolve, we provide ongoing support by monitoring your portfolio, tracking performance, and making adjustments to keep you on track.

As a fee-only fiduciary, our legal and ethical duty is to act in your best interest. Our recommendations are always based on what's best for you, not on earning a commission. This commitment ensures your personalized asset allocation is designed for one purpose: helping you achieve your financial goals.

Conclusion

Building lasting wealth comes from a disciplined, personalized investment strategy—not from chasing hot stocks or trying to time the market. The ideal portfolio is one that truly aligns with your unique goals, timeline, and comfort with risk.

Remember, your strategy isn't static. It requires periodic review and rebalancing to stay on course as your life and the markets change. By focusing on these core principles, you can build a resilient portfolio designed for long-term success.

Putting these principles into practice is the most important step. If you're ready to create a comprehensive plan tailored to your financial life, the team at Endeavor Financial Group is here to help. We provide the professional guidance needed to build and manage a portfolio that works for you.

Frequently Asked Questions

What is a good asset allocation by age?

A common rule of thumb is the "rule of 110," where you subtract your age from 110 to find the percentage you should hold in stocks. However, this is just a starting point. A truly optimal allocation depends more on your individual risk tolerance and financial goals than just your age.

How often should I rebalance my portfolio?

Most experts recommend reviewing your portfolio for rebalancing either annually or whenever a target allocation shifts by a predetermined amount, such as 5%. The right frequency depends on your portfolio's volatility and your tolerance for deviation.

What is the difference between asset allocation and diversification?

Asset allocation is about the mix between different asset classes (like stocks, bonds, and cash). Diversification is about spreading investments within each of those classes (for example, buying stocks in many different industries and countries).

What are the main asset classes to include in a portfolio?

The core asset classes are stocks (equities) for growth, bonds (fixed income) for stability and income, and cash or cash equivalents for liquidity and safety. Alternative investments like real estate can also be added for further diversification.

How does my risk tolerance impact my asset allocation?

A higher risk tolerance allows for a greater allocation to growth assets like stocks, which have higher potential returns but also more volatility. A lower risk tolerance requires a higher allocation to more stable assets like bonds and cash to preserve capital.

Can I create a custom portfolio on my own?

Yes, though it requires significant research and discipline. A financial advisor can add value through expert tax-planning strategies, behavioral coaching during market volatility, and ensuring your investments align with your broader financial goals.