Understanding the difference between a fiduciary and a non-fiduciary advisor is one of the most important steps you can take, especially if you're a business owner or nearing retirement. This choice directly impacts the advice you receive, the fees you pay, and whether your interests truly come first. Shockingly, a recent FINRA Foundation survey found that only 20% of investors have ever checked a financial professional's background with a regulator.

This article will cut through the confusion. We’ll break down the key differences between these two standards, explain the legal obligations behind them, and give you a clear framework for choosing the right partner for your financial journey.

TL;DR: Fiduciary vs. Non-Fiduciary

- A fiduciary advisor is legally required to act in your best financial interest.

- A non-fiduciary only has to recommend "suitable" products, not the best ones.

- Fiduciaries are typically paid a fee to minimize conflicts of interest.

- Non-fiduciaries can earn higher commissions by selling certain products over others.

- Always ask a potential advisor to confirm their fiduciary status in writing.

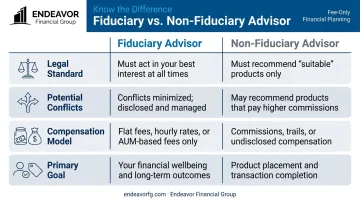

Fiduciary vs. Non-Fiduciary: A Quick Comparison

This side-by-side comparison highlights what separates an advisor legally bound to your best interests from one who isn't.

Legal Standard

- Fiduciary: Held to the highest legal standard of care, requiring them to act in the client's best interest.

- Non-Fiduciary: Must only ensure recommendations are "suitable" based on a client's objectives, risk tolerance, and financial situation.

Potential for Conflicts of Interest

- Fiduciary: Legally required to avoid or clearly disclose all potential conflicts of interest.

- Non-Fiduciary: Can be incentivized to recommend products with higher commissions, even if a better, less expensive option exists for the client.

Typical Compensation Models

- Fiduciary: Typically compensated through transparent, fee-only models (e.g., hourly rates, flat retainers, or a percentage of assets under management).

- Non-Fiduciary: Often commission-based or "fee-based." They can earn money from selling specific investment or insurance products, creating a potential conflict.

Who They Are

- Fiduciary: Registered Investment Advisers (RIAs) and Certified Financial Planner™ (CFP®) professionals are held to a fiduciary standard. This includes firms like Endeavor Financial Group.

- Non-Fiduciary: Broker-dealers and insurance agents have historically been held to the lower suitability standard.

What Is a Fiduciary Financial Advisor? The "Best Interest" Standard

A fiduciary financial advisor has a legal and ethical obligation to put your financial interests first. Think of it like a doctor's duty to a patient or a lawyer's duty to a client—their recommendations must be based solely on what is best for you, without regard for their own compensation.

This isn't just a promise; it's a legal requirement established under the Investment Advisers Act of 1940. This law holds fiduciaries to a high standard of trust and transparency, ensuring their advice is untainted by conflicts of interest.

Core Benefits of Working with a Fiduciary

Choosing a fiduciary advisor brings several key advantages, especially when making critical decisions about retirement or a business.

- Receive objective advice tailored to your unique goals, not an advisor's potential commission.

- Gain full transparency into fees and any potential conflicts of interest, building trust and eliminating hidden agendas.

- Benefit from holistic planning that focuses on a long-term strategy for your entire financial picture, not just on selling a product.

How Fiduciary Advisors Are Paid

The fee-only compensation model is the bedrock of the fiduciary standard. It aligns the advisor's success directly with the client's. Common structures include:

- A percentage of assets under management (AUM), typically 0.5% to 1.5% annually.

- A flat annual or quarterly retainer for ongoing financial planning and advice.

- An hourly rate for specific financial planning projects or consultations.

This model removes the temptation to recommend high-commission products, ensuring the advice you receive is truly in your best interest.

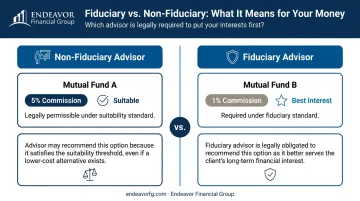

The Alternative: The "Suitability" Standard

The suitability standard is a lower bar. It requires that an investment recommendation must simply be "suitable" for a client's financial situation, goals, and risk tolerance. However, it does not require the recommendation to be the best or most cost-effective option available.

Here’s a practical example. An advisor operating under the suitability standard could have two nearly identical mutual funds to recommend:

- Mutual Fund A: A suitable fund that pays the advisor a 5% commission.

- Mutual Fund B: A nearly identical, slightly better-performing fund that only pays a 1% commission.

Under the suitability standard, the advisor can legally recommend Mutual Fund A because it is "suitable," even though Mutual Fund B would be in the client's best interest. A fiduciary, in contrast, would be legally obligated to recommend Mutual Fund B.

Understanding Potential Conflicts of Interest

The primary issue with the suitability standard is the inherent conflict of interest created by commission-based compensation.

Advisors might be incentivized to recommend:

- Proprietary Products: Funds or products created by their own firm, which may not be the best in the market.

- Investments with Higher Payouts: Mutual funds, annuities, or insurance products that offer higher commissions to the salesperson.

- Different Share Classes: Some funds have multiple share classes with varying fee structures, and an advisor might recommend the one with a higher sales charge.

Not all non-fiduciary advisors provide bad advice. However, the structure itself creates a potential for conflict that consumers must be aware of. To make matters more confusing, some advisors are "dual-registered." This means they can act as a fiduciary for advisory services but switch to a suitability standard when selling a specific product.

This dual role makes it crucial for you to ask for clarity on which standard they are operating under for any specific recommendation.

How to Choose the Right Advisor for You

Vetting a potential financial advisor is one of the most important financial decisions you'll make. Here is an actionable guide to help you find a true partner for your future.

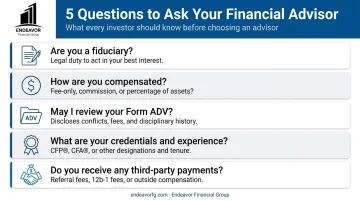

Key Questions to Ask Any Potential Advisor

Don't be afraid to ask direct questions. Any trustworthy professional will be happy to answer them clearly.

- "Are you a fiduciary at all times when working with me?" Get a "yes" and ask for it in writing.

- "How are you compensated? Are you fee-only, fee-based, or commission-based?" This reveals potential conflicts of interest.

- "Can you provide me with a copy of your Form ADV Part 2?" This is a disclosure document that registered investment advisors must file with the SEC, detailing their services, fees, and any conflicts of interest.

- "What are your credentials and certifications?" Look for designations like CFP® (Certified Financial Planner™) or CFA® (Chartered Financial Analyst), which require adherence to high ethical standards.

- "Do you or your firm receive any third-party payments for recommending specific investments?" This question targets revenue-sharing arrangements and other hidden fees.

Where to Verify Credentials

You don't have to take their word for it. You can and should verify an advisor's status and disciplinary history using free public tools.

- FINRA's BrokerCheck: Use BrokerCheck to see the background and experience of brokers, brokerage firms, and some investment advisers.

- SEC's IAPD Website: The Investment Adviser Public Disclosure (IAPD) website provides access to an investment adviser's Form ADV.

When you look them up, check for their registration type (are they a Registered Investment Adviser or a broker-dealer?) and review any disclosed disciplinary actions.

Why a Fiduciary Approach Matters for Your Future

For pre-retirees and business owners, the stakes are simply too high to settle for conflicted advice. When planning for major life events like a secure retirement or a business succession, you need absolute confidence that your advisor is on your side.

This assurance of unbiased, client-first advice is a necessity for protecting your future.

Working with a firm built from the ground up on the fiduciary principle provides that clarity and confidence. It means trust is built on unbiased advice and a comprehensive plan tailored solely to your unique financial goals.

At Endeavor Financial Group, our team of CFP® and CFA® professionals is committed to this standard. If you're looking for a partner to help you navigate your financial future with integrity, we invite you to schedule a consultation.

Conclusion

The distinction is simple but profound: a fiduciary advisor is legally and ethically bound to act in your best interest, while an advisor held to a suitability standard is not. The best financial partnerships are built on a foundation of trust, transparency, and aligned interests.

Before committing to an advisor, ask them directly if they are a fiduciary. Verify their credentials, understand their compensation model, and choose a partner who is legally obligated to put your financial well-being first.

Frequently Asked Questions

Is a fiduciary better than a financial advisor?

A fiduciary is a type of financial advisor, but one held to a higher legal and ethical standard. Whether it's "better" depends on your need for legally-bound, conflict-free advice, which is critical for major financial decisions.

What is the average fee for a fiduciary financial advisor?

Fees vary, but fee-only fiduciaries often charge between 0.5% to 1.5% of assets under management (AUM) annually. Others may charge a flat annual retainer or an hourly rate for specific planning projects.

What is a red flag for a financial advisor?

Red flags include an unwillingness to state in writing that they are a fiduciary, a lack of transparency about fees and compensation, or high-pressure sales tactics pushing you toward a specific product.

How can I verify if a financial advisor is a fiduciary?

Ask them directly to state it in writing. You should also request their Form ADV disclosure document and check their credentials on the SEC's IAPD website to confirm they are a Registered Investment Adviser.

Are all CFP® professionals fiduciaries?

Yes. As of June 30, 2020, the CFP Board requires all Certified Financial Planner™ professionals to act as a fiduciary at all times when providing financial advice to a client.

What is the difference between a fiduciary standard and a suitability standard?

The fiduciary standard requires advice to be in the client's "best interest." The suitability standard only requires a recommendation to be "suitable" for their situation, which allows for potential conflicts of interest like recommending a product with a higher commission.