The answer is often yes. Many entrepreneurs pay more in taxes than necessary simply because they overlook legitimate deductions. Understanding and strategically using tax write-offs isn't about finding loopholes; it's a fundamental part of managing your business's financial health and improving your cash flow.

This guide will break down the most important tax deductions for small businesses. We'll explain how they work, what you need to claim them, and the best practices to ensure you're keeping more of your hard-earned money.

TL;DR: Key Tax Deductions for Small Businesses

- Key categories include operations, workspace costs, payroll, vehicle use, and travel.

- Meticulous record-keeping and separate bank accounts are essential best practices.

- Avoid mixing funds and poor documentation to prevent higher taxes and audit risks.

What Is a Small Business Tax Deduction?

A tax deduction, often called a "write-off," is a business expense you can subtract from your company's gross income. By lowering your income on paper, you reduce the amount of that income subject to taxes.

For an expense to be deductible, the IRS has a simple, two-part rule: it must be both ordinary and necessary.

- Ordinary: The expense is common and accepted in your specific industry or line of work.

- Necessary: The expense is helpful and appropriate for your business. It doesn't have to be indispensable, just something that helps you operate.

For example, a professional baker can deduct flour, sugar, and a new oven as ordinary and necessary expenses. However, a luxury sports car would fail the test—it's neither common nor truly necessary for baking cakes.

Why Are Tax Deductions Crucial for Your Business?

Understanding tax deductions goes beyond simple compliance—it's a key strategy that directly impacts your bottom line. Every valid expense you deduct lowers your net profit, which in turn reduces both your income and self-employment taxes.

Let's walk through a clear example.

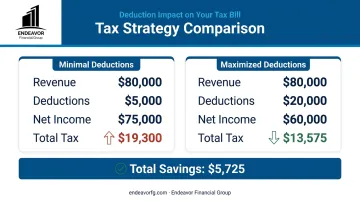

Imagine a freelance consultant generated $80,000 in revenue. They were busy and only tracked a few major expenses, totaling $5,000. Here’s their potential tax liability:

- Net Income: $75,000

- Estimated Self-Employment Tax (15.3%): ~$10,600

- Estimated Federal Income Tax (Single Filer): ~$8,700

- Total Estimated Tax: $19,300

Now, what if they take the time to find and categorize an additional $15,000 in legitimate deductions (home office, vehicle mileage, software subscriptions, phone bills, etc.)? The picture changes completely:

- Net Income: $60,000 ($80,000 revenue - $20,000 deductions)

- Estimated Self-Employment Tax (15.3%): ~$8,475

- Estimated Federal Income Tax (Single Filer): ~$5,100

- Total Estimated Tax: $13,575

By diligently tracking and claiming all their deductions, the consultant saves $5,725. That's cash that can be reinvested into the business, saved for retirement, or used to fund future growth.

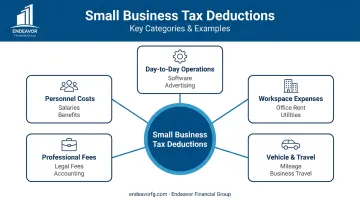

Key Categories of Small Business Tax Deductions

Deductions are easier to manage when you group them into logical categories. Here are the most common areas where small business owners can find savings.

Day-to-Day Operating Expenses

These are the costs required to keep your business running.

- Office Supplies & Software: Pens, paper, ink, and other standard office supplies are fully deductible. The same goes for software subscriptions essential to your business, like accounting software (QuickBooks), project management tools (Asana), or cloud storage (Dropbox).

- Advertising & Marketing: Any costs you incur to promote your business are 100% deductible. This includes digital ads on Google or social media, website hosting fees, printing business cards, and sponsoring local events.

- Phone & Internet: If you have a dedicated business phone line and internet service, you can deduct 100% of the cost. If you use your personal phone, you can only deduct the percentage of its use that is for business.

- Bank & Merchant Fees: Don't forget the small stuff. Monthly service fees for your business bank account and credit card processing fees from services like Stripe or Square are all deductible.

Workspace Expenses

Whether you rent a storefront or work from a spare bedroom, your workspace has deductible costs.

- Rent for Business Property: If you rent an office, co-working space, or retail location, the monthly rent is fully deductible.

- Home Office Deduction: To claim this, you must use a specific area of your home regularly and exclusively for business. You have two options for calculating it:

- Simplified Method: A straightforward calculation of $5 per square foot, capped at 300 square feet for a maximum deduction of $1,500.

- Actual Expense Method: A more complex calculation where you deduct a percentage of your actual home costs, including mortgage interest, rent, utilities, insurance, and repairs. This percentage is based on the size of your office relative to your home.

- Utilities: For a commercial space, electricity, water, and gas are fully deductible. For a home office, these costs are factored into the Actual Expense method.

Personnel & Professional Development Costs

Expenses related to your team and your own professional growth are valuable write-offs.

- Employee Salaries & Benefits: The wages, salaries, and bonuses you pay to employees are deductible. This also includes your share of their payroll taxes and contributions to their health insurance or retirement plans.

- Payments to Independent Contractors: The fees you pay to freelancers, consultants, or other non-employees for their services are fully deductible. Remember, if you pay a contractor $600 or more in a year, you must issue them a Form 1099-NEC.

- Professional Fees: You can deduct fees paid to accountants, lawyers, or business consultants for services related to your business. This includes fees for financial planning and wealth management services that guide your business strategy.

- Education & Training: Costs for courses, workshops, and industry publications that help you maintain or improve the skills needed for your current business are deductible.

Vehicle, Travel, and Meal Expenses

- Business Use of a Vehicle: You can deduct expenses for business vehicle use in one of two ways. Both methods require a detailed mileage log to support your claim.

- Standard Mileage Rate: The IRS sets a standard rate each year (it was 67 cents per mile for 2024), which you multiply by your business-related mileage.

- Actual Expense Method: Track and deduct a percentage of all your car-related costs, including gas, oil changes, repairs, insurance, and depreciation.

- Travel Expenses: For overnight business trips, you can deduct 100% of your costs for airfare, hotels, and rental cars.

- Business Meals: You can generally deduct 50% of the cost of qualifying business meals with clients, partners, or while traveling for business. Documentation is key: you must record who you met with, when, where, and the business purpose of the meal.

Capital & Financial Deductions

- Business Insurance: Premiums for general liability, professional liability (errors and omissions), and commercial property insurance are fully deductible.

- Interest on Business Loans: Interest paid on business loans, lines of credit, and business credit cards is deductible.

- Depreciation (Section 179 & Bonus Depreciation): When you buy a large asset like equipment, a vehicle, or furniture, you typically deduct its cost over several years through depreciation. However, special tax codes like Section 179 and Bonus Depreciation often allow you to deduct the entire cost in the year you buy it, providing a significant immediate tax benefit.

Other Important Deductions

- Self-Employed Health Insurance Premiums: Sole proprietors and partners can deduct 100% of the premiums they pay for health, dental, and long-term care insurance for themselves and their families.

- Retirement Plan Contributions: Contributions you make to a retirement plan for yourself, such as a SEP IRA or Solo 401(k), are deductible. This is a powerful way to lower your current tax bill while saving for the future. Contribution limits change annually (the SEP IRA limit for 2024 is $69,000), and a financial advisor can help you maximize this benefit.

- Qualified Business Income (QBI) Deduction: Owners of pass-through businesses (sole proprietorships, partnerships, S-corps) may qualify for this complex but valuable deduction, allowing you to deduct up to 20% of your qualified business income.

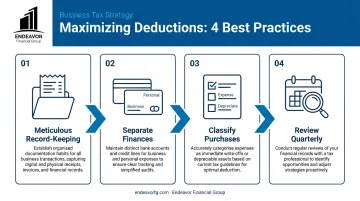

Best Practices for Maximizing Your Deductions

Finding deductions is only half the battle. Claiming them correctly requires good habits.

Meticulous Record-Keeping is Non-Negotiable

The IRS requires you to have proof for every deduction you claim, and the burden of proof is always on you, the taxpayer. This means keeping every receipt, invoice, and bank statement related to your business.

Using accounting software to digitize and categorize receipts as they come in is the best way to stay organized and audit-proof. According to the IRS, you must keep records that substantiate all your income and deductions.

Maintain Separate Business and Personal Finances

Commingling funds—using your personal bank account for business expenses or your business card for personal purchases—is a major red flag for the IRS. Open a dedicated business checking account and credit card from day one. This creates a clean, easy-to-follow paper trail that simplifies bookkeeping and legitimizes your business operations.

Understand the Difference Between Expensing and Depreciating

Knowing how to classify purchases is crucial. Small, consumable items like office supplies are "expensed," meaning you deduct their full cost in the year of purchase.

Large, long-lasting assets like machinery or office furniture are "capitalized." You deduct their cost over several years through depreciation, unless you use a provision like Section 179 to write them off immediately.

Review Your Expenses Quarterly

Don't wait until tax season to look at your numbers. Sit down with your bookkeeper or accountant each quarter to review your profit and loss statement. This helps you catch miscategorized expenses, spot financial trends, and find potential deductions.

This proactive review also helps your financial advisor coordinate effectively with your tax professional to align business deductions with your long-term wealth goals.

Common Mistakes to Avoid

- Mixing business and personal expenses. Writing off a family vacation for a single business call is a red flag. Always maintain strict separation between accounts.

- Forgetting small, recurring costs. A $15 monthly software fee adds up. These minor expenses can total hundreds in missed deductions annually, so track everything.

- Keeping poor or incomplete records. A credit card statement alone isn't enough proof. Support each deduction with a receipt, an invoice, and a note on its business purpose.

Conclusion: Turn Tax Deductions into a Financial Strategy

Understanding and tracking tax deductions is more than just a year-end chore; it's a fundamental part of running a financially healthy business. It ensures you pay your fair share of taxes—and not a penny more.

But tax planning is just one piece of the puzzle. The most successful business owners integrate their tax-efficient strategies with their long-term goals for retirement, investment, and business growth. This is where true financial confidence comes from.

While a CPA handles tax preparation, a financial advisor helps you see the bigger picture. This involves creating a holistic plan that aligns your tax strategy with your overall financial objectives.

The team at Endeavor Financial Group works with business owners to do just that. We help you structure your business finances to support both your company's growth and your personal vision for the future.

Frequently Asked Questions

Boost Your Deductions with Strategic Financial Planning

Request a quote and our experts will contact you within 24 hours with tailored solutions and pricing.

For immediate assistance, feel free to give us a direct call at 463-273-4062. You can also send us a quick email at team@endeavorfg.com.

For immediate assistance, feel free to give us a direct call at 463-273-4062. You can also send us a quick email at team@endeavorfg.com.