Tax-loss harvesting (TLH) is a strategy designed to plug that leak. In short, it’s the practice of selling investments at a loss to offset the taxes you owe on capital gains.

This guide provides a detailed roadmap for pre-retirees and dividend investors on how to apply this strategy to their portfolios in 2026. We'll cover the step-by-step mechanics, the unique rules that apply to dividend stocks, and the common pitfalls that can trip up even experienced investors.

Key Takeaways

- Sell investments at a loss to offset capital gains and up to $3,000 of ordinary income.

- Reduce the tax burden on portfolios that generate regular, taxable dividend income.

- Sell a losing position and replace it with a similar, but not identical, investment after 30 days.

- Avoid the wash sale rule, which can be triggered by automatic dividend reinvestments (DRIPs).

What Is Tax-Loss Harvesting for Dividend Stocks?

Tax-loss harvesting is a tax-efficiency strategy designed to lower your investment tax bill. Instead of aiming for new returns, the goal is to sell an investment that has decreased in value to "harvest" or realize a capital loss.

You can then use this harvested loss to offset capital gains elsewhere in your portfolio. The IRS requires you to follow a specific order:

- Short-term losses first offset short-term gains.

- Long-term losses first offset long-term gains.

- Any remaining losses can then offset gains of the other type.

If your total capital losses exceed your total capital gains, the IRS allows you to use up to $3,000 of the excess loss to reduce your ordinary income (like your salary or business income). Any remaining losses can be carried forward to future tax years.

This is the inverse of "tax-gain harvesting." That strategy involves intentionally selling winning investments during a low-income year to lock in gains at a low tax rate and reset your cost basis higher.

Why This Strategy Matters for Dividend Investors in 2026

A portfolio built around dividend stocks is designed to generate regular income. But every dividend payment is a taxable event, creating a consistent tax drag that can reduce your total return. Tax-loss harvesting provides a way to counteract this effect.

The primary benefit is using unrealized losses in some of your holdings to offset realized gains from others. For example, if you sell a high-growth tech stock for a large profit, you can simultaneously sell a dividend stock that's temporarily down to neutralize the tax bill.

While tax laws for 2026 could see adjustments, the principle of offsetting gains with losses is a cornerstone of the U.S. tax code. Proactive tax planning remains critical regardless of minor shifts in tax brackets.

According to the IRS, after offsetting all capital gains, you can deduct up to $3,000 in losses against ordinary income each year. This rule has remained consistent for decades.

How Tax-Loss Harvesting Works: A Step-by-Step Guide

Executing a tax-loss harvesting strategy requires careful attention to detail. Here’s a breakdown of the process.

Step 1: Identify and Analyze Losing Positions

First, scan your taxable brokerage account for any stocks, ETFs, or mutual funds that are trading below your cost basis. These are your potential candidates for harvesting.

However, don't just sell blindly. Analyze why the position is down. Is it a quality company caught in a temporary market downdraft, or has something fundamentally changed for the worse?

Selling a good long-term holding for a small tax benefit might be a poor trade-off. The goal is to harvest losses from investments that no longer fit your strategy or are in a temporary dip you can strategically exit.

Step 2: Sell the Asset to "Harvest" the Loss

Once you've identified a good candidate, you simply sell the security. This action formally "realizes" the capital loss, making it available for tax purposes. It's crucial to document the sale date, the cost basis, the sale price, and the total amount of the loss for your records.

Step 3: Manage the Wash Sale Rule and Reinvest

This is the most critical step. The IRS "wash sale rule" prevents you from claiming a loss if you buy a "substantially identical" security within 30 days before or after the sale (a 61-day window).

To stay compliant while keeping your money in the market, you have two main options:

- Wait and Repurchase: If you still believe in the stock, wait 31 days before buying it back. The primary risk is missing a potential rebound during the waiting period.

- Reinvest in a Similar Asset: To maintain market exposure, immediately reinvest in a different but similar security. For example, you could sell an individual energy stock like Exxon Mobil and buy a broad energy sector ETF. According to IRS Publication 550, stocks of different corporations are generally not considered substantially identical.

Step 4: Report the Loss on Your Tax Return

Finally, you'll report your harvested losses on your tax return. All your capital gains and losses are reported on IRS Form 8949, and the net results are then transferred to Schedule D to calculate your final capital gains tax.

Key Rules and Challenges for Dividend Stocks

Tax-loss harvesting a dividend portfolio presents unique challenges that demand careful attention.

The Wash Sale Rule and Dividend Reinvestment Plans (DRIPs)

This is the number one pitfall for dividend investors. Many investors use DRIPs to automatically reinvest their dividends back into the same stock. However, the IRS considers this reinvestment a "purchase."

If you sell a stock for a loss, but your DRIP automatically buys even a small number of new shares within the 30-day window, the IRS will disallow the loss. This can happen before or after your sale.

Actionable Tip: If you plan to tax-loss harvest a specific stock, temporarily turn off the DRIP for that security well in advance. You can collect the dividend as cash and manually reinvest it after the 61-day wash sale window closes.

Qualified Dividend Holding Periods

Qualified dividends are taxed at lower long-term capital gains rates, but they come with a condition. You must have held the stock for more than 60 days during the 121-day period that begins 60 days before the ex-dividend date.

If you sell a stock to harvest a loss before meeting this holding period, any recent dividend you received from it will be reclassified as a non-qualified dividend. This means it will be taxed at your higher ordinary income rate, which could easily wipe out the tax benefit of the harvested loss.

The Risk of "Tax-Driven" Selling

It can be tempting to sell a stock just to capture a tax loss, but this can be a mistake. Investment fundamentals should always come first, as a falling stock price might be a sign of deeper problems with the company.

Selling a high-quality, dividend-growing company you believe in for a minor tax benefit is often a poor long-term decision. Remember, tax-loss harvesting is an optimization tool, not the primary driver of your investment strategy.

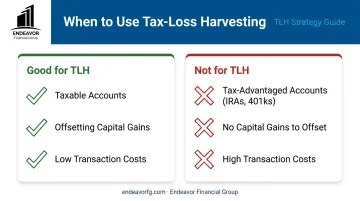

When Tax-Loss Harvesting May Not Be a Good Fit

TLH is a powerful tool, but it's not right for every situation. It's generally not effective or appropriate in these cases:

- In tax-advantaged accounts: There are no capital gains taxes in accounts like IRAs or 401(k)s, so there's nothing to offset. TLH only applies to taxable brokerage accounts.

- If you have no capital gains: If you don't have any capital gains to offset, the benefit is limited to the $3,000 deduction against ordinary income.

- If transaction costs are too high: If the commissions or fees to sell and repurchase securities are higher than your potential tax savings, it's not worth it.

Why Professional Guidance Is Crucial for Tax-Loss Harvesting

While the concept of tax-loss harvesting is simple, the execution is complex. The nuances of the wash sale rule, DRIPs, and qualified dividend holding periods create numerous opportunities for costly mistakes. A misstep can not only negate the tax benefit but also attract unwanted attention from the IRS.

At Endeavor Financial Group, we integrate tax-efficiency strategies like TLH into our comprehensive financial planning. We don't just look at your portfolio at the end of the year; our five-step process ensures we are monitoring for these opportunities proactively.

Our disciplined approach includes:

- Discovery & Analysis: We start by understanding your complete financial picture to identify potential tax-saving opportunities.

- Strategic Implementation: Our team executes trades while carefully managing wash sale rules and dividend schedules.

- Ongoing Monitoring: We proactively watch your portfolio throughout the year, not just at year-end.

This process ensures that your tax strategy is perfectly aligned with your long-term financial goals, helping you keep more of your hard-earned money.

Frequently Asked Questions

What are the tax-loss harvesting limits and rules for 2026?

There is no limit to the amount of capital losses you can use to offset capital gains. After canceling out all gains, you can deduct up to $3,000 of losses against your ordinary income per year. Any remaining losses can be carried forward to future years indefinitely.

How will dividends be taxed in 2026?

Qualified dividends are taxed at lower long-term capital gains rates (0%, 15%, or 20%), while non-qualified dividends are taxed as ordinary income. These rates are expected to continue but are always subject to potential legislative changes.

How should I invest $1 million to retire on dividend income?

A $1 million dividend portfolio requires diversification across high-quality stocks, ETFs, and REITs. Advanced strategies like asset location and tax-loss harvesting are essential to minimize taxes and preserve capital. A financial advisor can create a personalized plan for your needs.

Can I do tax-loss harvesting in my 401(k) or IRA?

No. Tax-loss harvesting is only for taxable investment accounts, like a standard brokerage account. Since transactions within retirement accounts like 401(k)s and IRAs do not generate taxable events, there are no gains or losses to report.

What is the difference between tax-loss harvesting and tax-gain harvesting?

Tax-loss harvesting involves selling investments at a loss to offset gains and reduce your tax bill. Conversely, tax-gain harvesting means selling assets at a gain during a low-income year to lock in a 0% or low tax rate and reset your cost basis.